$4B Maple Finance Charges 70bps Vs Wall Street’s 2-and-20

Key Points

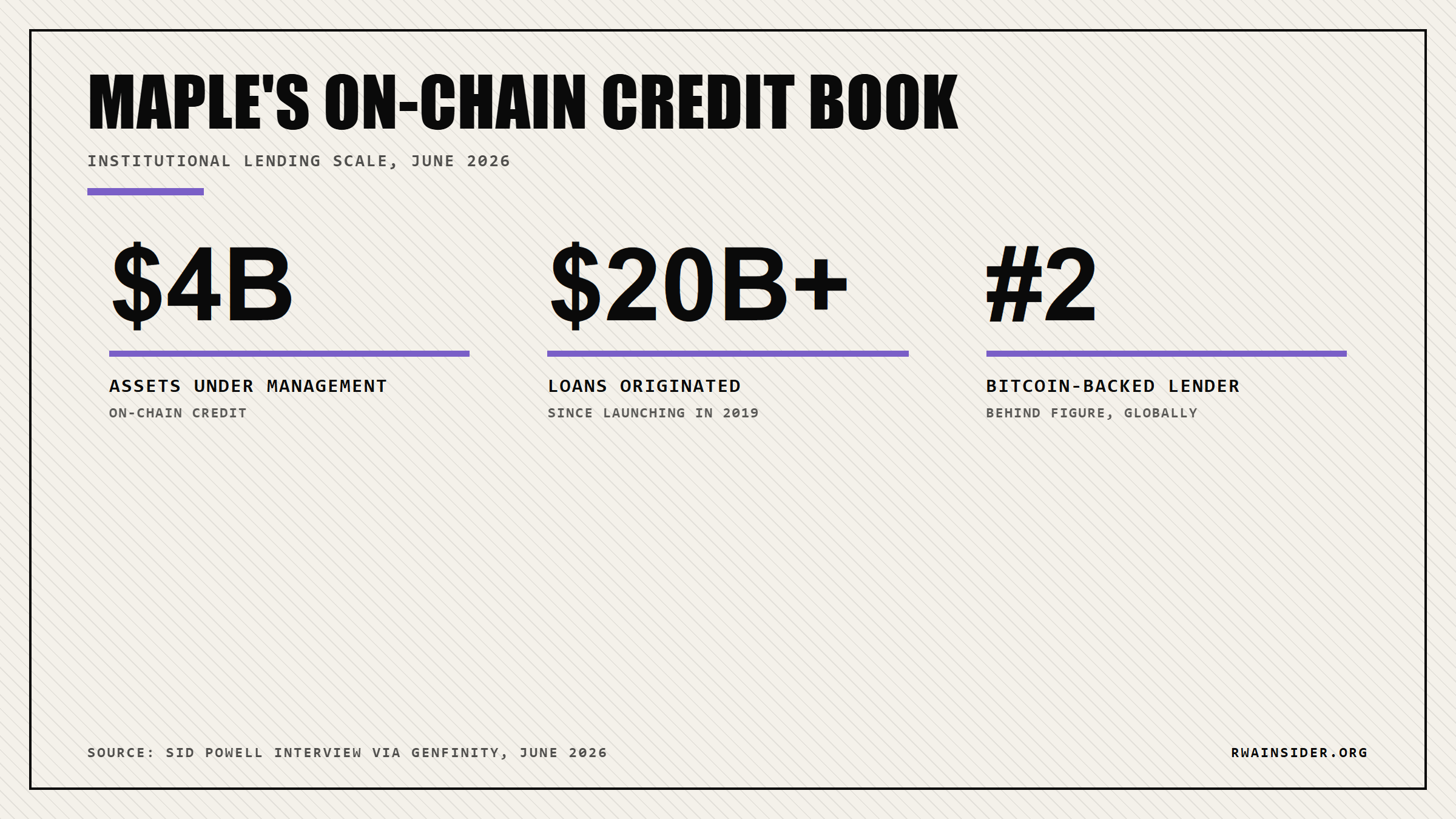

- Maple Finance now manages over $4 billion in on-chain credit and has originated more than $20 billion in loans since launching in 2019.

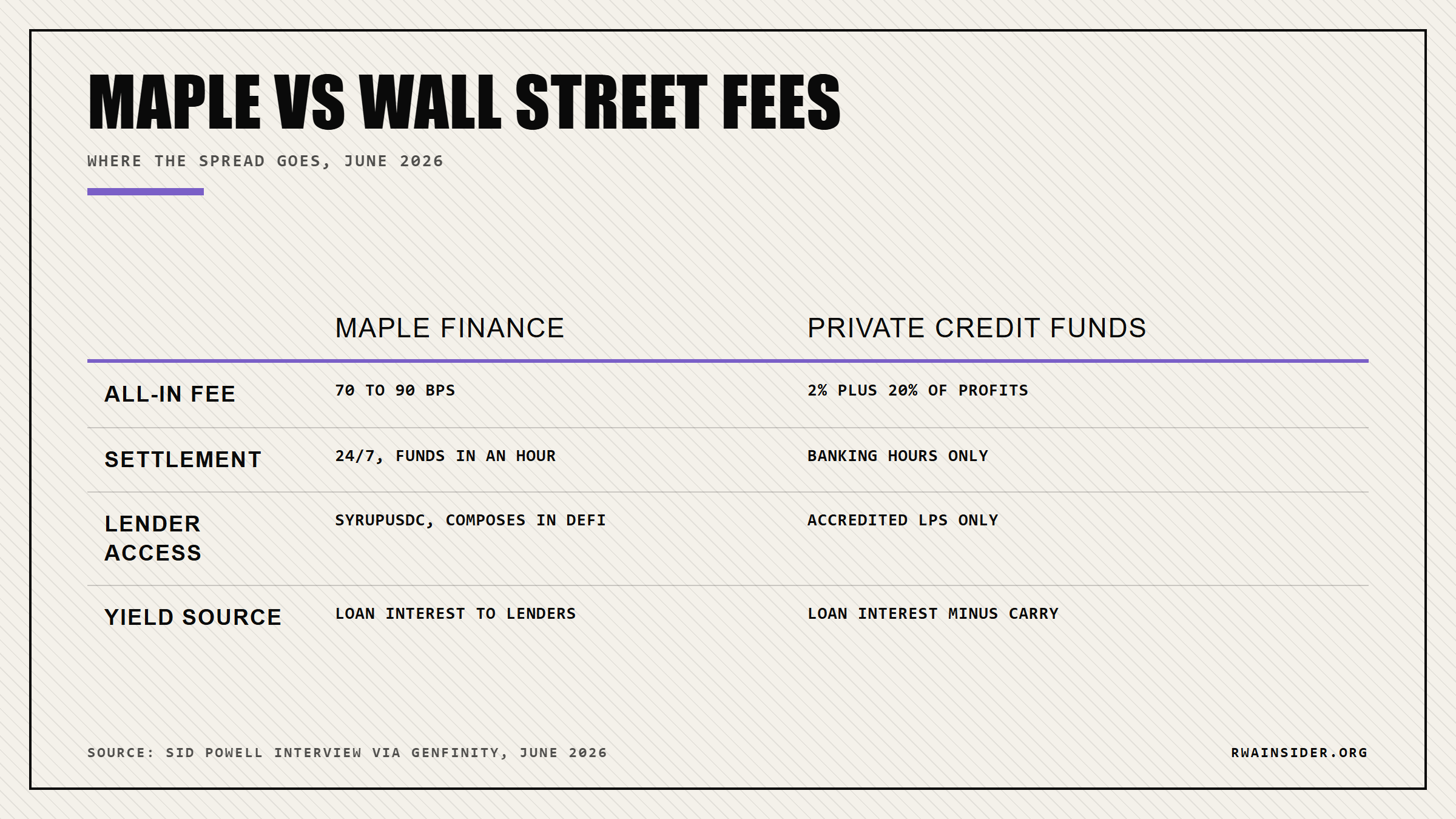

- The protocol charges 70 to 90 basis points all-in versus the 2-and-20 model private credit funds use, sending the saved spread to lenders.

- A wallet can hold syrupUSDC, now $3.02 billion in size, to earn that loan interest and post it as collateral on Aave or Morpho.

Maple Finance now runs more than $4 billion in on-chain credit, lending to trading firms and asset managers against Bitcoin, ETH, Solana, and XRP. Co-founder Sid Powell laid out the scale in an interview with Genfinity, which summed up the pitch in four words: “Their Margin Is Our Lunch.” Strip away the institutional framing and the real story is a fee model that pays lenders, because the same loan interest that funds those tickets flows to anyone holding syrupUSDC, no allowlist required.

Maple Finance Lends $4B Against Bitcoin Collateral

Maple Finance has become one of the largest institutional lenders in crypto, managing more than $4 billion in assets.

Powell positions it as an on-chain asset manager, not a retail DeFi app.

Since launching in 2019 the protocol has originated over $20 billion in loans, including more than $11.27 billion in 2025 alone, with second-quarter revenue last year up 154%.

The borrowers are crypto-native institutions: trading firms, asset managers, and exchanges, with ticket sizes from $10 million to $500 million.

Maple takes Bitcoin, ETH, Solana, and XRP as collateral, which makes it the second-largest global lender against Bitcoin, behind Figure.

Speed is the product.

Late last year a borrower called on a Thursday for a $500 million loan, moved $750 million in Bitcoin into tri-party custody, and the stablecoins funded within an hour, settling that Saturday.

Borrowing costs sit near 6% annualized, and collateral stays in tri-party custody, so a family office can raise working capital without selling Bitcoin or triggering a tax event.

Where syrupUSDC’s $3B Yield Comes From

The lender side is where a wallet actually plugs in.

Maple’s syrupUSDC reached $3.02 billion in size by the end of 2025, with syrupUSDT crossing $1.12 billion.

The yield is real loan interest paid by institutional borrowers, not token emissions, which is the difference between a durable rate and a temporary farm.

That token composes across DeFi.

Maple has wired syrup yield into Aave, Sky, and Morpho, and expanded the products to Base, Solana via Kamino, and BNB Chain.

The fee math is the real story.

Private credit funds charge a 2-and-20 model, a 2% management fee plus 20% of profits, while Maple charges 70 to 90 basis points all-in.

For a DeFi user, that gap matters less as a swipe at Wall Street than as basis points that land in a syrupUSDC holder’s yield instead of a fund manager’s pocket.

Against the roughly 2.1% a wallet earns supplying USDC on permissionless Aave, that loan-interest yield is the spread worth tracking in the wider on-chain credit and protocol race.

Maple’s Real Rivals Are KKR And Blackstone

Sid Powell, co-founder of Maple Finance, argues the competition is not other DeFi protocols.

It is Ares, KKR, and Blackstone, the private credit giants that cannot yet handle stablecoins, tokenized collateral, or round-the-clock settlement.

Maple already operates natively across all three.

Powell calls fee compression the clearest adoption signal, the same way on-chain marketplaces charge 2 to 3% against eBay’s 10 to 20%.

He expects Bitcoin-backed lending to grow tenfold by 2028, reaching $200 billion, and wants Maple to pass Figure for the top spot.

The collateral is coming to meet it: Figure has already tokenized billions of dollars of home-equity loans, the kind of paper Maple plans to lend against next.

New deployments on Tempo, Arc, and Canton are on the roadmap, alongside earn programs for the neobanks and fintechs now holding stablecoin balances.

For a wallet, the open question is access: the borrowing side stays gated to vetted institutions, but the syrupUSDC that funds it already trades and composes across DeFi.

Whether Maple takes the top Bitcoin-backed lending spot from Figure depends on how long banks stay on the sidelines, and the next few quarters of originations will tell. For a wallet, the question is simpler: that 70-to-90 basis point fee floor only matters if the loan interest keeps reaching syrupUSDC without an allowlist.

For the mechanics behind the lender-side token, see how Maple redirects a quarter of its revenue into SYRUP buybacks, then weigh whether syrupUSDC’s loan-interest yield earns a place in your wallet.

Frequently Asked Questions

What is syrupUSDC and how does it earn yield?

syrupUSDC is Maple Finance’s yield-bearing stablecoin token, which reached $3.02 billion in size by the end of 2025. Its yield comes from real interest that institutional borrowers pay on loans, not from token emissions, and the token can be supplied into Aave, Sky, and Morpho.

How much does Maple Finance charge compared to private credit funds?

Maple charges 70 to 90 basis points all-in. Traditional private credit funds run a 2-and-20 model, a 2% management fee plus 20% of profits. That gap flows to lenders as higher yield rather than to a fund manager.

Can I lend on Maple Finance without an institutional account?

The borrowing side is gated to vetted institutions, with ticket sizes from $10 million to $500 million. The lender side is different: the syrupUSDC token trades and composes across DeFi, so a wallet can gain exposure on secondary markets and use it as collateral on Aave or Morpho.

How does Maple Finance compare to Figure in Bitcoin-backed lending?

Maple is the second-largest global lender against Bitcoin, behind Figure, with borrowing costs near 6% annualized. Co-founder Sid Powell expects Bitcoin-backed lending to grow tenfold by 2028 to $200 billion and wants Maple to take the top spot.