Maple Routes 25% Revenue To SYRUP Buybacks After $36M Scar

Key Points

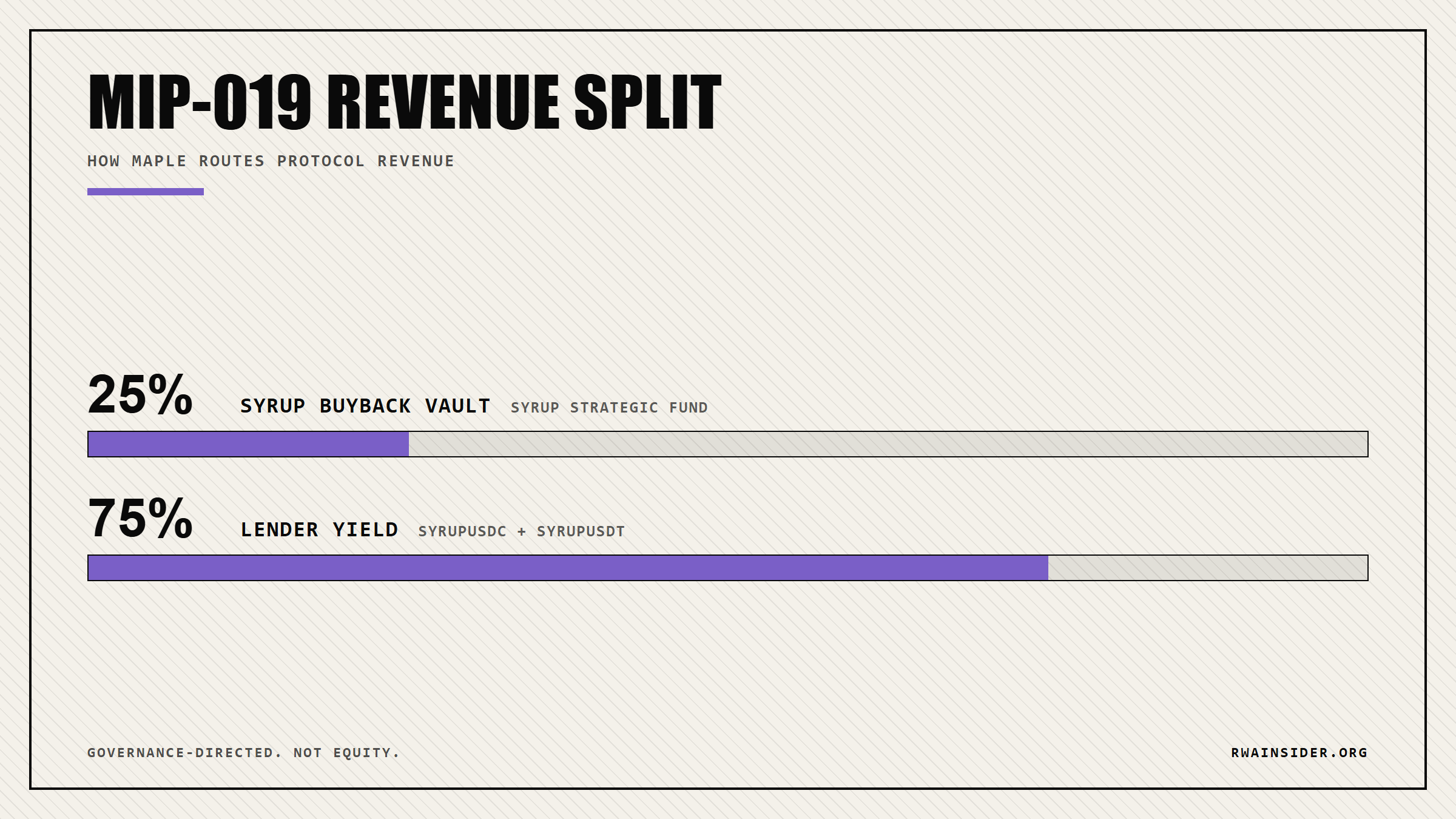

- Maple Finance now sends 25% of protocol revenue into SYRUP token buybacks under the MIP-019 governance proposal.

- The active Maple token is SYRUP, not the legacy MPL ticker that closed migration in May 2025 at a 1:100 conversion.

- DeFi users can buy SYRUP on Uniswap without KYC, or hold syrupUSDC to plug a wallet directly into Maple’s institutional credit yield.

Maple Finance’s SYRUP token now routes 25% of protocol revenue into onchain buybacks under the MIP-019 governance proposal. Crypto Daily framed the model as the underrated RWA play on May 21, 2026, calling Maple’s institutional credit business the misread sibling of the tokenized Treasury narrative. For a wallet holding $1,000 in stablecoins, the question is whether to buy SYRUP on Uniswap for buyback exposure or hold syrupUSDC for credit yield from Maple’s institutional loan book.

Maple Routes 25% Of Revenue Into SYRUP Buybacks On Uniswap

Crypto Daily wrote that “the bigger question is not whether Maple has a catchy RWA label.”

The publication argued the active token is SYRUP, not the long-dead MPL ticker still surfacing in price-tracker search results.

Maple governance approved MIP-019 to allocate 25% of ongoing protocol revenue to the Syrup Strategic Fund for buybacks and DAO balance sheet growth.

SYRUP trades on Uniswap, Binance, Coinbase, Kraken, KuCoin, and Gate.io. The MPL-to-SYRUP migration ran at a 1:100 ratio and closed in May 2025.

Crucially, SYRUP is not a fee token like a DEX governance token. It is a governance and ecosystem token tied to Maple Finance‘s onchain asset-management business.

The token economics are a step beyond pure emissions, but they are not equity. SYRUP holders direct value through governance votes, not legal claims on Maple revenue or assets.

How syrupUSDC Routes Wallets Into Maple’s Institutional Loan Book

syrupUSDC and syrupUSDT are yield-bearing stablecoins that give DeFi wallets access to Maple’s institutional lending strategies. They are not the same as holding plain USDC.

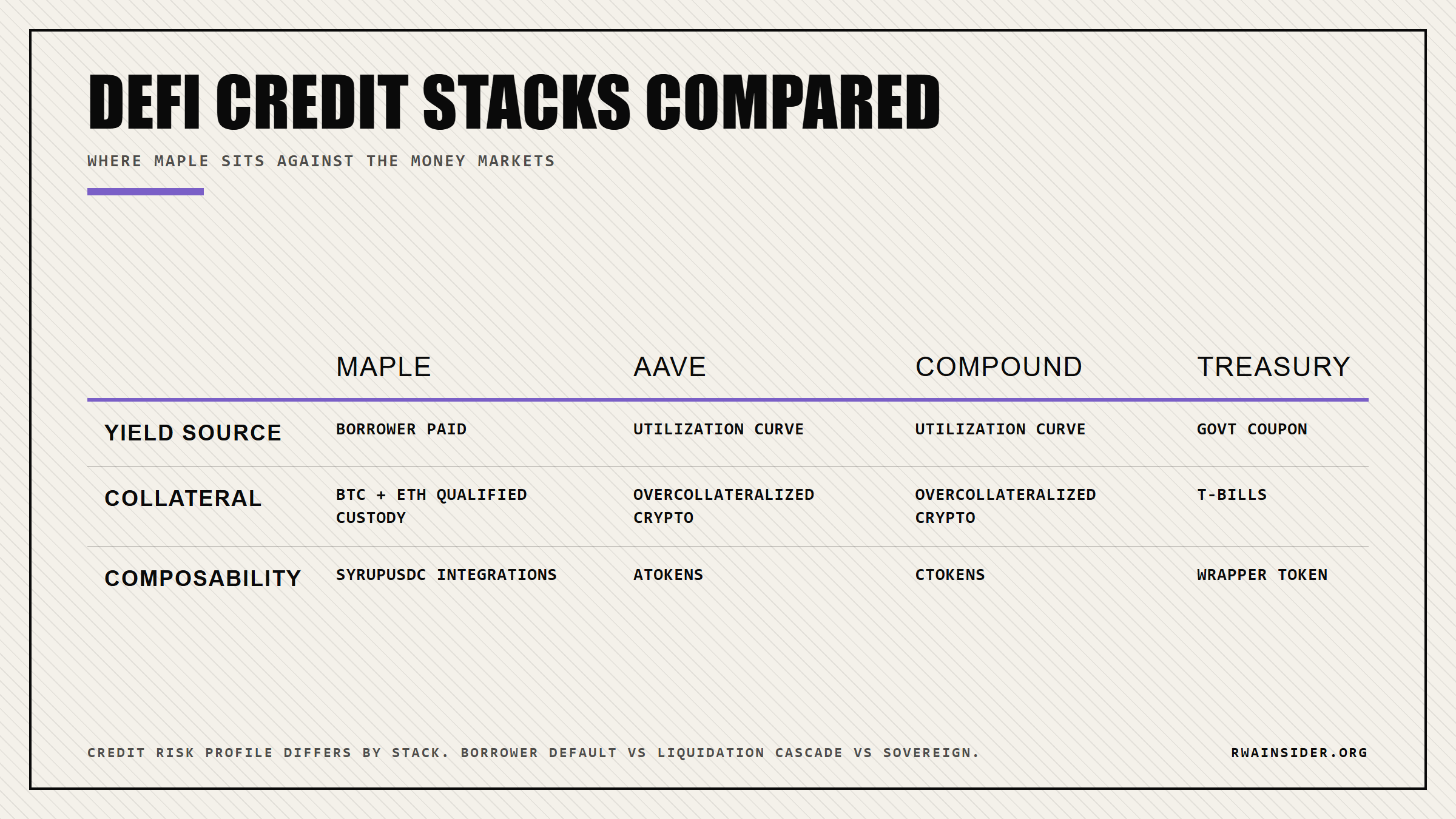

Maple’s lender documentation says interest is set by loan terms through credit underwriting and risk management, not algorithmic utilization curves.

That is closer to traditional private credit than to Aave or Compound money markets.

The Blue Chip Secured Pool accepts BTC and ETH collateral held in qualified custody, with active margin management. Borrowers are institutional, not retail wallets.

For a DeFi user, this matters less as a private-credit institution story than as a stablecoin yield product that finally has revenue-linked token economics behind it.

Readers can compare yields across DeFi-native RWA tokens as more secured pools come online.

The yield comparison is harder to pin than for tokenized Treasury wrappers.

Maple does not publish a fixed APY for syrupUSDC because returns track the underlying loan book, not a published reference rate.

Distribution matters as much as yield.

If syrupUSDC integrates as collateral inside other DeFi protocols, the asset gets composable beyond Maple’s front-end, which is the on-chain distribution Maple needs to scale SYRUP buybacks.

The $36M Orthogonal Default That Still Defines Maple’s Risk Stack

Private credit is not risk-free.

In December 2022, Orthogonal Trading defaulted on about $36 million of Maple-linked loans after FTX-related stress, and Maple severed ties with the firm over alleged misrepresentation.

Maple’s newer secured pool is more conservative, but “conservative does not mean immune,” as the protocol’s own risk framing puts it.

Anyone holding syrupUSDC should review the borrower base, collateral types, and liquidation process before depositing.

Maple’s Token Transparency Framework states that SYRUP “does not represent equity ownership in any Maple legal entity and does not provide explicit legal rights to assets or revenues.”

Value accrual is governance-directed, not contractual.

Regulatory risk sits behind every layer.

Tokenized credit overlaps with securities, lending, stablecoin, and asset-management rules, and access can change quickly by jurisdiction.

Maple’s lender documentation flags that Maple products may not be available to all users, and future compliance updates could change the syrupUSDC product entirely.

The framework notes Maple scored 37 out of 40 in the Blockworks Token Transparency report from June 2025, a useful differentiator in altcoin markets where many projects publish limited disclosure.

Whether SYRUP earns the “underrated” label depends on whether Maple’s secured loan book grows without another Orthogonal moment. The next quarter of revenue prints will be the tell.

Track more Protocol Battles coverage from RWA Insider as the tokenized credit stack matures.

Frequently Asked Questions

What is SYRUP and how does it differ from the old MPL token?

SYRUP is Maple Finance’s active governance and utility token. It replaced MPL through a 1:100 conversion that closed in May 2025. SYRUP captures 25% of Maple’s protocol revenue through onchain buybacks, while MPL is legacy terminology that still surfaces in older price trackers.

Where can I buy SYRUP without KYC?

SYRUP trades permissionlessly on Uniswap, which means any wallet can swap into it without identity verification. Maple’s own token page also lists Coinbase, Binance, Kraken, KuCoin, and Gate.io, but those routes require exchange KYC.

Does syrupUSDC offer a higher yield than Aave USDC?

Maple does not publish a fixed APY for syrupUSDC. The rate is set by loan terms through credit underwriting, not algorithmic utilization curves like Aave or Compound. The trade-off is borrower credit exposure in return for potentially less-correlated yield.

Is Maple Finance safe after the 2022 $36 million Orthogonal default?

Maple’s Blue Chip Secured Pool now accepts only BTC and ETH collateral held in qualified custody, with active margin management. That model is more conservative than the unsecured Orthogonal Trading exposure that defaulted in December 2022, but credit, liquidity, smart contract, and custody risk all remain on the table.