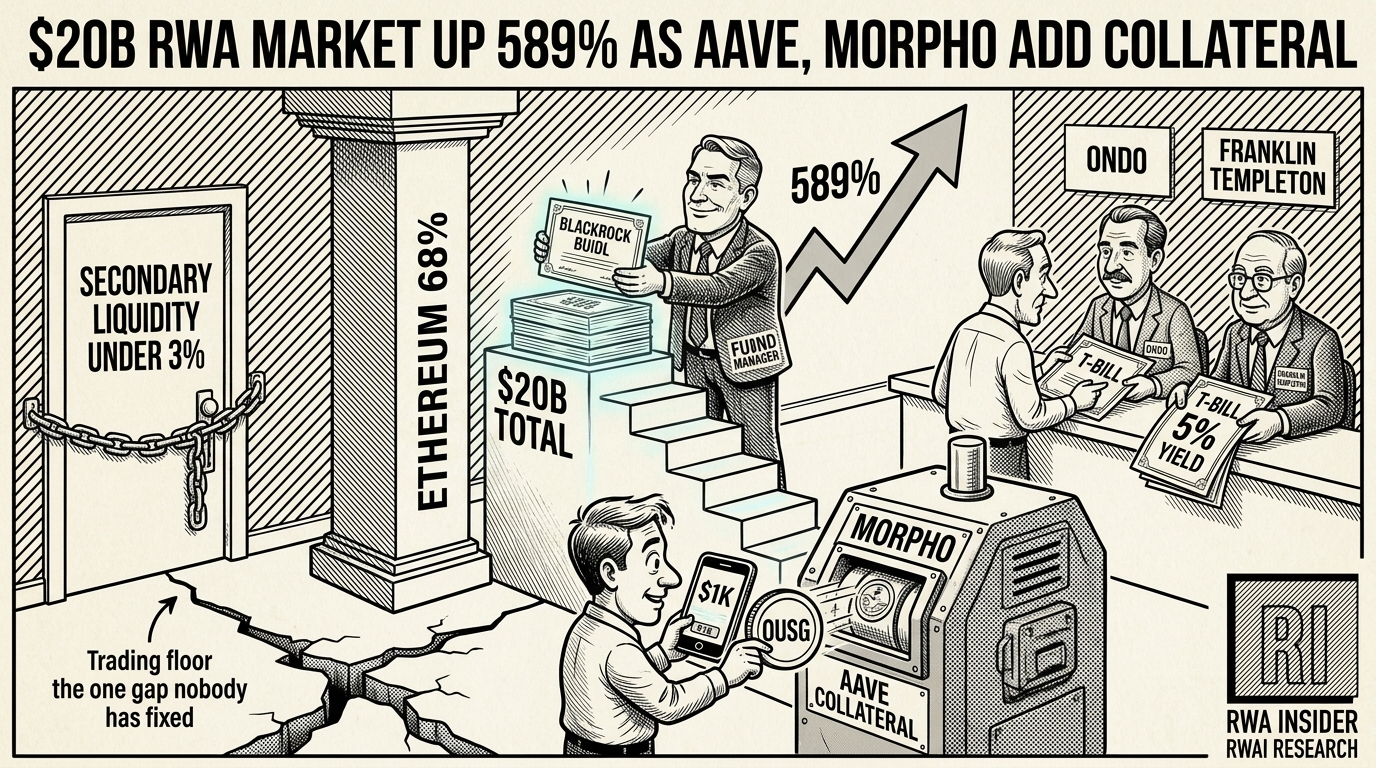

$20B RWA Market Up 589% As Aave, Morpho Add Collateral

Key Points

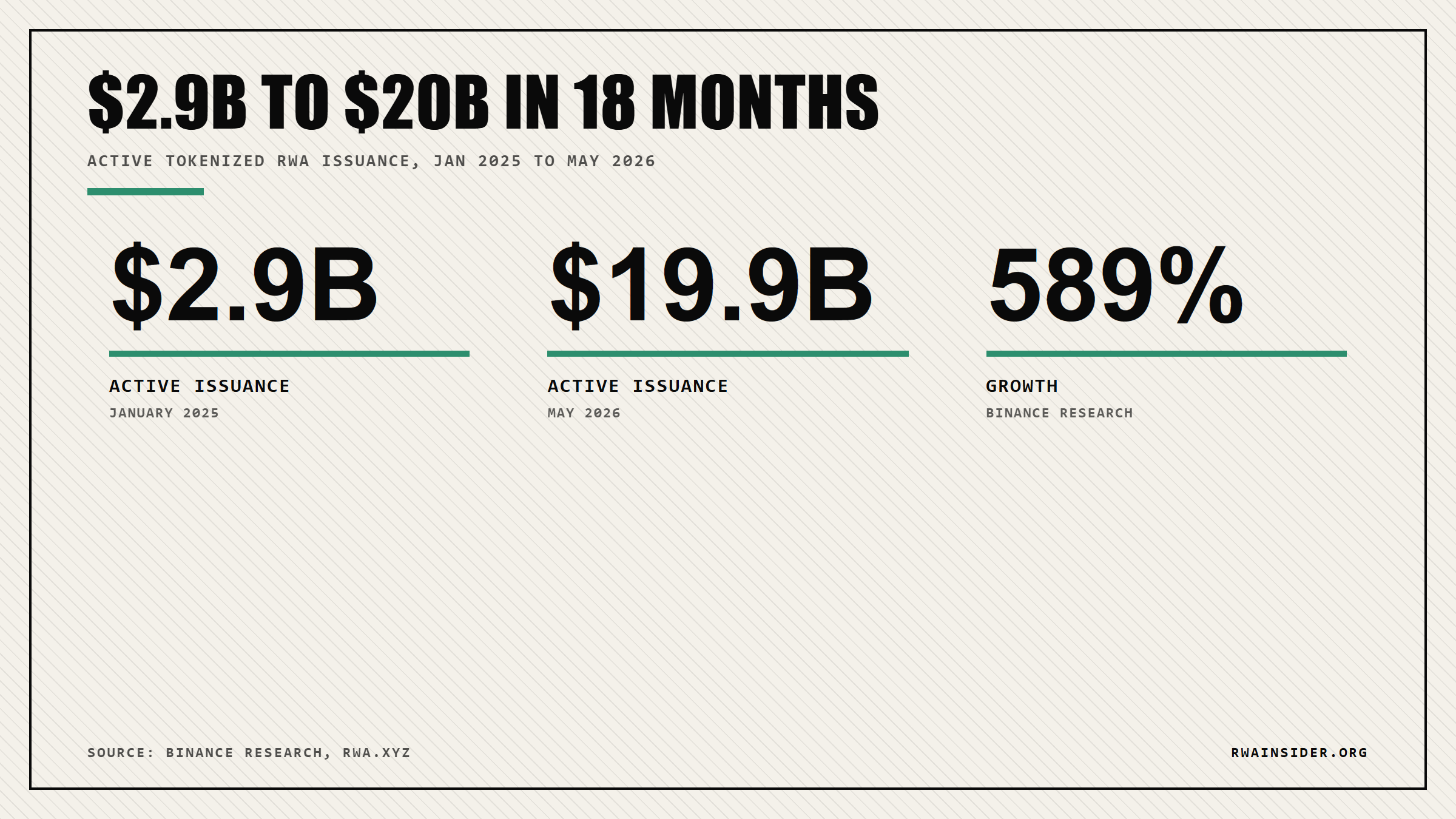

- Binance Research data shows active tokenized RWA issuance jumped 589% in 2026, climbing from $2.9 billion in early 2025 to nearly $20 billion by May.

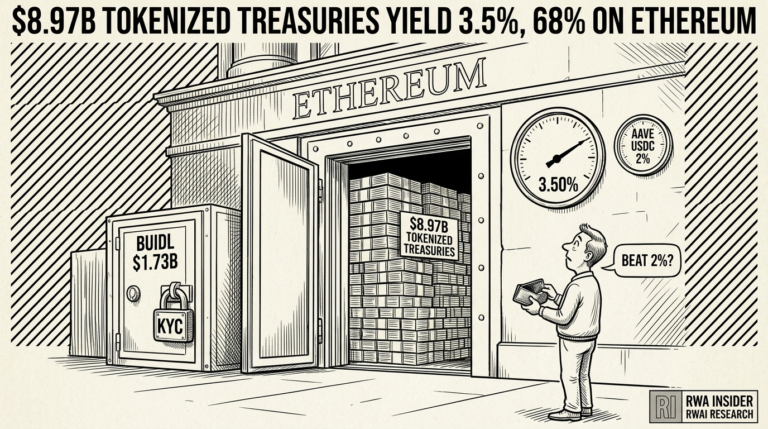

- Tokenized US Treasuries lead at about $9.6 billion, with BlackRock’s BUIDL at $1.7 billion and Ondo Finance’s OUSG and USDY at $850 million combined.

- A $1,000 wallet can hold PAXG gold permissionlessly today, while OUSG and Morpho open Treasury-backed borrowing to anyone who clears one-time KYC.

Active tokenized real-world assets surged 589% this year, climbing from $2.9 billion in early 2025 to nearly $20 billion by the end of May 2026. Binance Research published the figure in its mid-2026 review, formally calling 2026 the sector’s “maturation year” even as Bitcoin slid below $65,000. For anyone running a wallet, the number that matters is not the headline growth but where those assets now sit: tokenized Treasuries earning roughly 5% have become live collateral inside Morpho and Aave, turning idle stablecoins into borrowing power.

The 589% Surge Crossed $20 Billion By May

Binance Research measured active tokenized RWAs, not the loose market cap that folds in stablecoins. Active issuance means verified collateral, disclosed custody, and real redemption.

On that tighter basis the sector opened 2025 near $2.9 billion, almost all of it tokenized US Treasuries.

By the end of May 2026 it had crossed $19.9 billion, a 589% jump in 18 months.

The catalyst was BlackRock and its BUIDL fund, launched on Ethereum in March 2024 and now the largest tokenized money market fund at $1.7 billion.

Its clean regulatory run lowered the risk barrier for every issuer that followed.

Tokenized Treasuries and private credit drove almost all of the gain. Real estate and commodities together are still under 8% of issuance.

Most of this issuance lands on Ethereum, which hosts roughly 68% of active RWA value. That is the chain where Aave, Morpho, and Compound already run.

Where Tokenized Treasuries Pay 5% Into Morpho

Tokenized US Treasuries are the engine. They stood at roughly $9.6 billion on 30 May 2026, nearly half of all active issuance.

Ondo Finance runs the largest non-BlackRock book, with OUSG and USDY at $850 million combined. Franklin Templeton’s BENJI token adds $700 million.

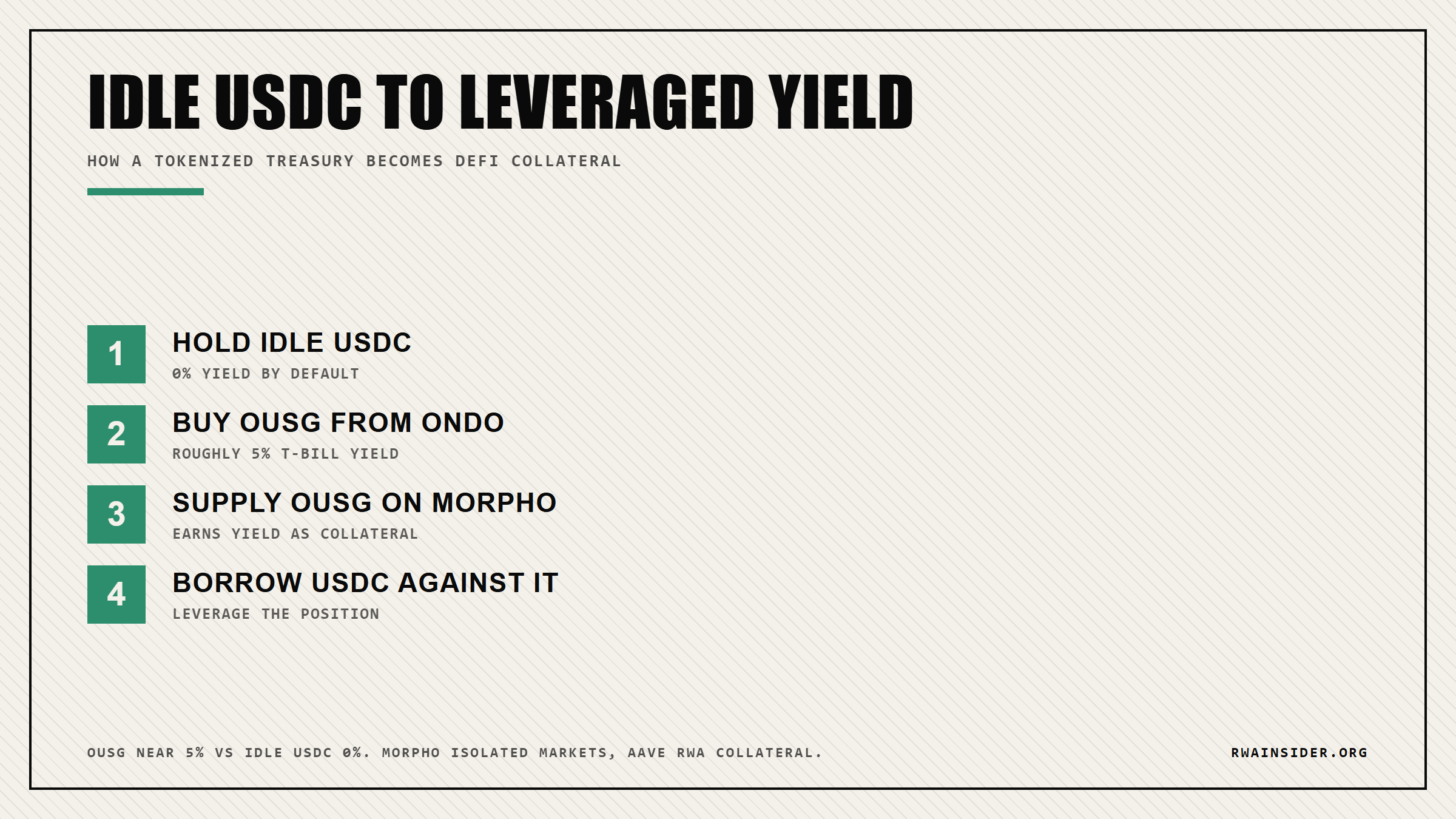

The pull is simple. Stablecoins sitting in DeFi earn nothing by default, while a tokenized T-bill pays roughly 5% and stays composable.

That is where the collateral story starts. Morpho’s isolated markets let a wallet borrow USDC against OUSG, and Aave governance has approved RWA-backed tokens as a collateral class.

Strip away the maturation-year language and this is the real shift: a tokenized Treasury stops being a parking spot and becomes borrow power you can leverage on-chain.

Private credit is the faster-growing tier off a smaller base. Centrifuge, Maple, and Goldfinch pushed tokenized credit TVL to $4.1 billion, up from $1.2 billion at the start of 2025.

You can compare yields across tokenized treasuries before deciding where idle stablecoins should sit.

Secondary Liquidity Stays Under 3% Of Issuance

The primary market matured fast. The secondary market did not.

Tokenized Treasuries dodge the problem because the issuer redeems them for dollars within a business day, which substitutes for market depth.

Everything else trades thin. For tokenized private credit, secondary turnover runs below 3% of outstanding issuance a year, by the estimate of Standard Chartered’s digital asset research group.

That is a private-fund liquidity profile, not a public-market one. Fractional ownership lowered the ticket size; it did not create buyers.

Concentration is the other catch. The top four Treasury issuers, BlackRock, Ondo, Franklin Templeton, and Superstate, control more than 85% of that $9.6 billion market.

For a wallet, the risk is contagion: if a tokenized credit pool defaults the way several Goldfinch borrower pools did in 2022, the loss now cascades into the Aave and Morpho markets holding that paper.

Ondo Global Markets and Backed Finance are both building venues to deepen that secondary book through 2026.

That is why DeFi protocols cap RWA collateral with governance-set concentration limits.

The issuance race is basically settled. Whether tokenized RWAs become assets you can exit, and not just enter, is what the next year of secondary-market plumbing decides.

Watch the gap between primary growth and exit liquidity, and see how the same tokenized funds that were once walled off from public DeFi are now turning into collateral.