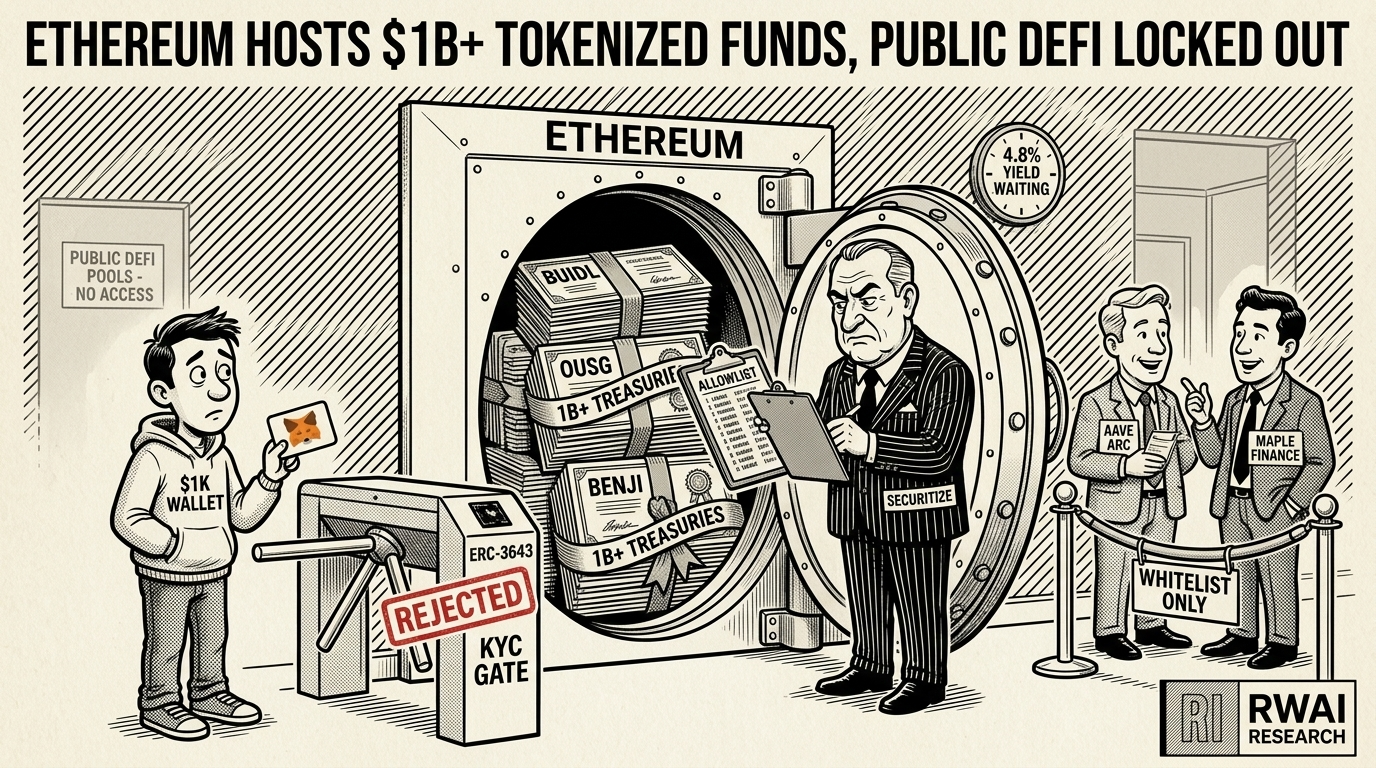

Ethereum Hosts $1B+ Tokenized Funds, Public DeFi Locked Out

Key Points

- Tokenized U.S. Treasury products on Ethereum have crossed the $1 billion mark, anchored by BlackRock’s BUIDL and Ondo Finance’s OUSG share classes.

- Permissioned standards including ERC-3643 and ERC-4626 encode KYC and transfer rules at the token contract, so unverified wallets get blocked by default.

- A retail wallet holding $1k cannot deposit BUIDL or OUSG directly into Aave or Compound, because transfer logic rejects any non-allowlisted address.

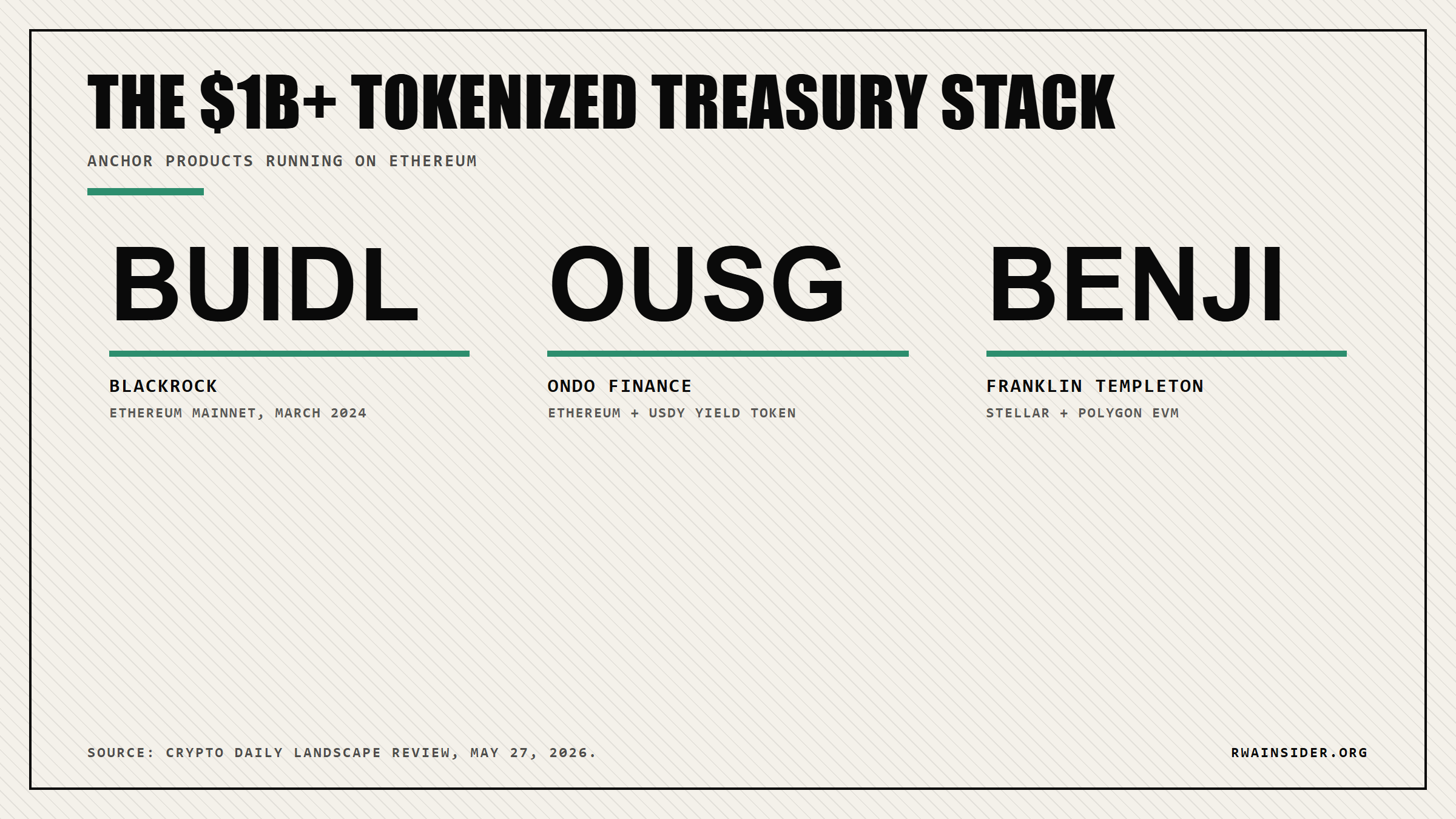

Tokenized U.S. Treasury funds have crossed the $1 billion mark, and almost every credible product runs on Ethereum or an EVM-compatible chain. Crypto Daily mapped the landscape on May 27, 2026, writing that “Ethereum continues to be the default venue for issuance, custody, and settlement, especially when institutions are involved,” with BlackRock’s BUIDL, Ondo Finance’s OUSG, and Franklin Templeton’s BENJI as the anchor products. For a wallet holder on MetaMask, the catch is direct. These tokens live on Ethereum but cannot be deposited into Aave or Compound, because their transfer logic blocks any address not pre-approved by the issuer’s allowlist.

The $1B+ Treasury Stack Behind The Ethereum Lead

Crypto Daily’s analysis pulls together what allocators already track: tokenized Treasury funds are no longer pilots. BlackRock launched BUIDL on Ethereum mainnet in March 2024 with Securitize as the SEC-registered transfer agent, and the product set the template for share registries that live onchain.

Ondo Finance followed with OUSG and the yield-bearing USDY, both primarily on Ethereum.

Franklin Templeton’s OnChain U.S. Government Money Fund started on Stellar but added Polygon for broader EVM interoperability.

Even when issuers pick a different chain for distribution, the canonical share registry typically stays on Ethereum because that is where custody integrations, audit firms, and transfer agents already work.

ERC-3643 And The Wallet That Cannot Touch OUSG

Stripped down to standards, two ERCs do most of the gatekeeping. ERC-3643, the renamed T-REX framework, enforces identity checks and transfer rules at the token contract level, meaning a transfer to an unverified wallet reverts.

ERC-4626 standardizes the vault interface used by some funds and yield products, which helps DeFi integrations but does not unlock permissioned tokens by default.

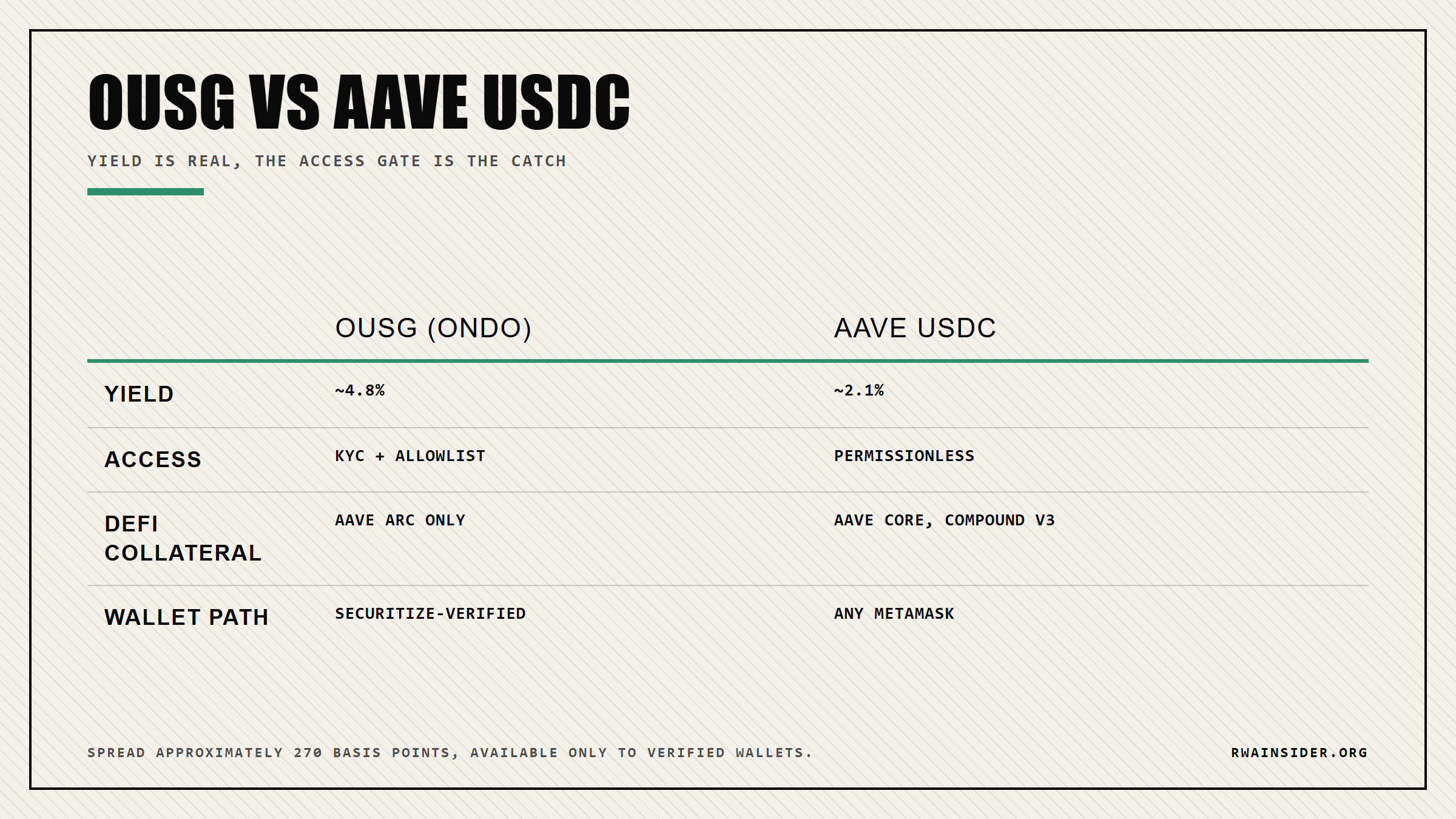

The yield available on these instruments is real. OUSG pays roughly 4.8% from short-term Treasuries, against roughly 2.1% on Aave USDC at current utilization, a spread of around 270 basis points.

The catch is access. For a DeFi user with $1k in MetaMask, OUSG and BUIDL cannot be deposited as collateral on Aave Core, Compound V3, or any public pool that has not been allowlisted by the issuer.

Strip away the press release and this is really about wallets paying for KYC clearance to reach Treasury yield, not about whether Ethereum hosts the asset.

Readers can explore more RWA Insider coverage of tokenized fund market structure as the standards converge.

The path that works today is indirect: hold BUIDL through Securitize after KYC, then loop the position through wrappers that some funds approve on a venue-by-venue basis.

What Aave Arc And Multichain Wrappers Could Open Next

The forward indicator to watch is which permissioned venues actually start clearing flows.

Aave’s institutional pools, commonly referred to as Aave Arc, sit on Ethereum and were built to give allowlisted addresses controlled access to lending markets. Institutional credit platforms including Maple Finance and Clearpool Institutional also center their activity on Ethereum and provide named credit lines rather than open pools.

None of these are accessible to a wallet without a verified identity.

The second indicator is multichain. As RWA Insider previously covered, BlackRock has already extended BUIDL to Solana, Aptos, Arbitrum, Avalanche, Optimism, and Polygon, while keeping the canonical share registry on Ethereum mainnet through Securitize, BUIDL’s transfer agent.

If Ondo opens its USDY wrapper to permissionless secondary trading on a wider set of EVM L2s, retail DeFi gets one of the first real on-ramps to Treasury yield without an allowlist gate.

Until that happens, the $1 billion in tokenized Treasury supply remains a custodial pool with a public chain underneath it.

Whether Ondo opens a non-KYC USDY wrapper on a major L2, or BUIDL allows broader DeFi composability through Securitize’s permission engine, decides if Treasury yield reaches the average MetaMask wallet by year-end.

Compare how RWA Insider tracks the BUIDL wrapper architecture that already routes into Morpho DeFi liquidity for a step-by-step view of how the indirect path clears today.

Frequently Asked Questions

What is BlackRock’s BUIDL fund and which chain does it run on?

BUIDL is BlackRock’s tokenized money market fund holding cash, U.S. Treasury bills, and repurchase agreements. The product launched on Ethereum mainnet in March 2024 with Securitize as the SEC-registered transfer agent. BUIDL has since extended to Solana and several EVM L2s while keeping the canonical share registry on Ethereum.

Can I deposit OUSG to Aave as collateral?

Not on Aave’s public pools. Ondo Finance’s OUSG token uses permissioned transfer rules that block any address that has not passed Ondo’s KYC and allowlist process. Aave Arc, the institutional-only pool, can support tokens like OUSG but is itself gated to allowlisted addresses.

What yield does OUSG pay compared to stablecoin DeFi?

OUSG pays roughly 4.8% from short-term Treasuries, versus roughly 2.1% on Aave USDC at current utilization, a spread of around 270 basis points. The yield gap is real but only available to wallets that complete Ondo’s KYC process and hold the token through a supported custodian.

Why does ERC-3643 matter for retail DeFi access?

ERC-3643, also known as T-REX, encodes identity checks and transfer rules inside the token contract itself, so a transfer to an unverified wallet reverts at the protocol level. Tokens built on permissioned standards like ERC-3643 cannot be sent into general DeFi pools without the issuer extending the allowlist to the pool contract.