$25B Threshold: New York Rule Bans Stablecoin Yield

Key Points

- NYDFS proposed a stablecoin rule on June 10, 2026, banning rehypothecation and any interest paid to holders, aligned with the federal GENIUS Act.

- Issuers with more than $25 billion outstanding must hold an extra 0.5% of reserves at insured banks, capped at $500 million.

- The interest ban hits issuer rewards like Coinbase’s USDC program, not the yield a wallet earns lending USDC on Aave or Morpho.

New York’s financial regulator wants to rewrite the rules for stablecoin issuers, and one line matters most for a wallet: the draft introduces “a ban on paying interest to stablecoin holders.” The New York Department of Financial Services, or NYDFS, proposed the rule on June 10, 2026, aligning it with the federal GENIUS Act, according to The Block. For DeFi, the translation is narrower than the headline sounds. This targets issuer-paid rewards, not the yield your wallet earns lending USDC on Aave, while tighter reserve rules quietly cut depeg risk.

NYDFS Bans Stablecoin Interest And Rehypothecation

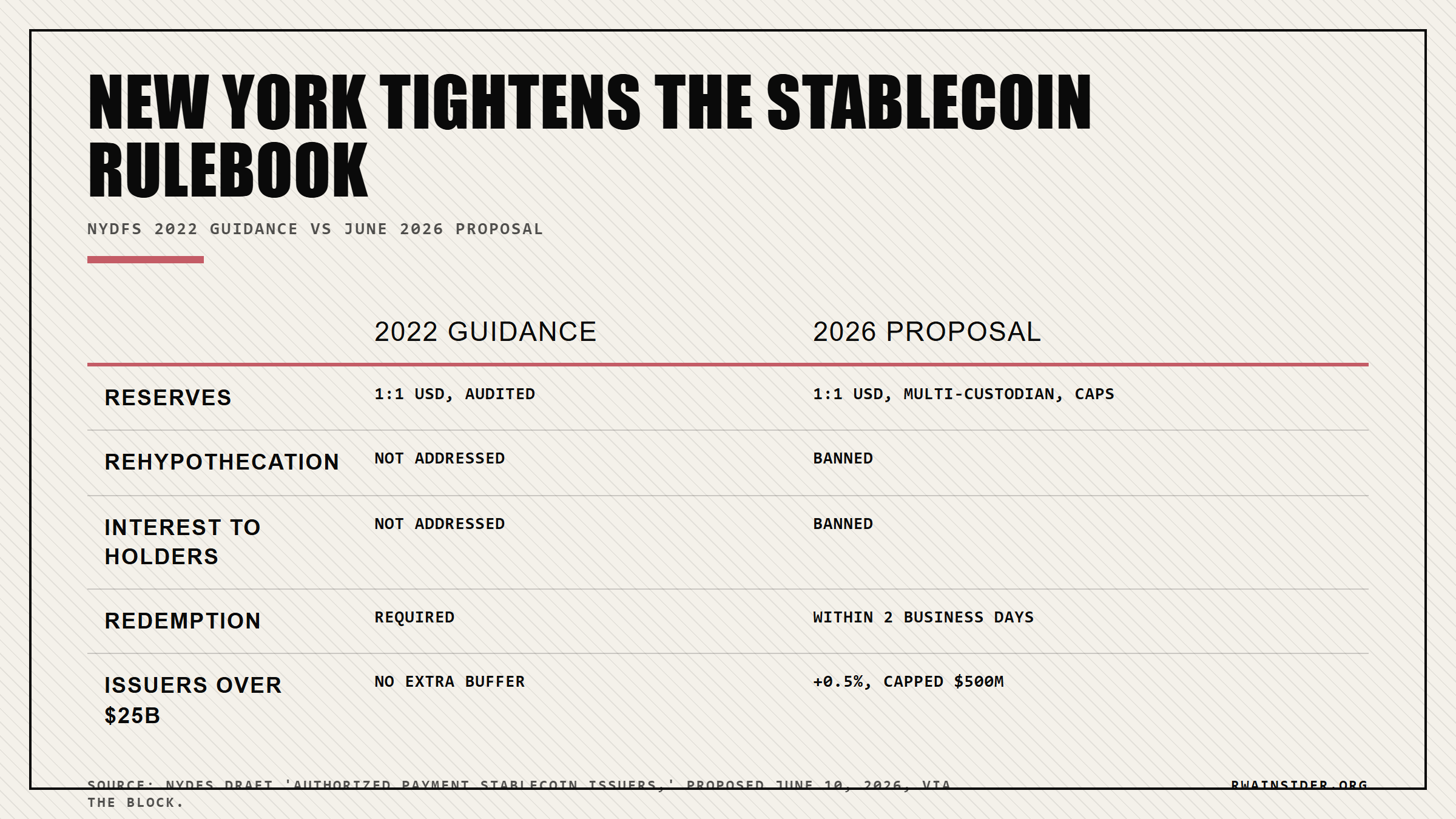

The New York Department of Financial Services published a draft rule titled “Authorized Payment Stablecoin Issuers” on June 10, 2026, first reported by The Block.

It builds on the state’s 2022 stablecoin guidance and keeps the basics: one-to-one dollar reserves, guaranteed redemption, and independent audits.

The new teeth are what matter. Reserves must sit across multiple custodians with concentration limits, rehypothecation is banned, and issuers cannot pay interest to token holders.

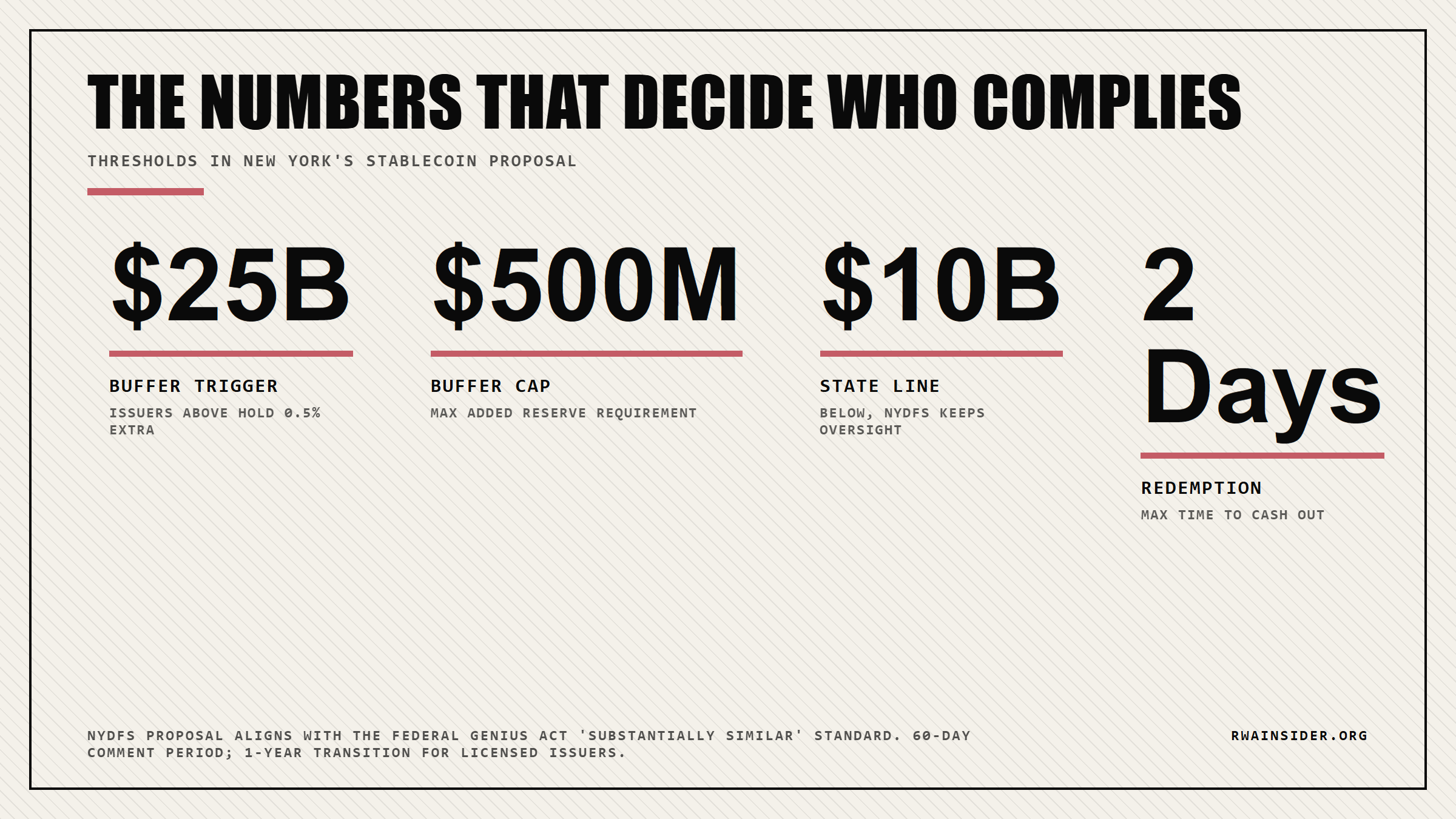

Redemptions must clear within two business days, and the whole framework is written to pass the federal GENIUS Act’s “substantially similar” standard.

None of this is live yet. The draft entered a 10-day pre-proposal window followed by a 60-day public comment period, with a one-year transition for licensed issuers.

For on-chain users, the headline reads scarier than the reality, and the whole difference comes down to who is actually paying the yield.

Your Aave Yield Survives, Issuer Rewards May Not

Start with the ban that sounds most alarming: no interest to stablecoin holders. That rule targets the issuer, not the lending market.

When you lend USDC on Aave or Morpho, the yield comes from borrowers paying to borrow, not from Circle cutting you a check. That income stream is untouched.

What the rule squeezes is issuer-paid rewards, the kind of program that pays you simply for parking a token in a wallet or on an exchange.

Strip away the regulatory language and this is really about killing the hold-our-coin-collect-a-rate model, while leaving permissionless DeFi yield alone.

The capital rules bite higher up. Issuers with more than $25 billion outstanding must park an extra 0.5% of reserves at insured banks, capped at $500 million.

NYDFS also wants to keep supervising issuers under $10 billion, a sign US stablecoin oversight is heading toward a two-layer state and federal split rather than one national license.

If you want to follow how new stablecoin rules reshape on-chain yield, those thresholds are where the next fights happen.

What The $25B Buffer Means For USDC And USDT

USDC and USDT both sit far above the $25 billion line, so they absorb the extra buffer without breaking stride. The pressure lands on smaller issuers.

A token issuer with a thin balance sheet now faces multi-custody costs, higher audit frequency, and that 0.5% capital drag. Some will not clear the bar.

That matters for liquidity. The stablecoins that survive the rules are the ones that stay listed, stay deep on DEXs, and stay usable as collateral.

The interest ban is not new ground either. RWA Insider has covered how the issuer-yield ban already left a Coinbase-shaped loophole, with rewards routed through an affiliate rather than the issuer itself.

Fintech analyst Zennon Kapron, writing in Forbes, flagged that gap months ago, and the NYDFS draft does not obviously close it. BlackRock, for its part, formally objected to the federal reserve restrictions back in May.

The next signals to watch are concrete: whether the final GENIUS Act text matches these thresholds, and whether New York’s licensed issuers have to rebuild their custody stacks to stay compliant.

Whether this reshapes your wallet depends on the fine print of the final GENIUS Act text, and the next sixty days of comments will set it. Until then, the rules that protect your stablecoin and the rules that limit its rewards are moving in lockstep.

The stablecoins worth holding through this are the ones with clean reserves, fast redemption, and deep on-chain liquidity. Keep watching which issuers clear the new bar.

Frequently Asked Questions

Does New York’s stablecoin rule ban the yield I earn on Aave or Morpho?

No. The ban applies to issuers paying interest to people who simply hold the token. The yield you earn lending USDC on Aave or Morpho comes from borrowers, not the issuer, so it is untouched by this rule.

Which stablecoins are affected by the $25 billion threshold?

USDC and USDT both sit well above $25 billion, so they must hold the extra 0.5% reserve buffer, capped at $500 million. Smaller issuers stay below the line but face the new custody and audit costs instead.

When would the New York stablecoin rules take effect?

Not immediately. The draft runs through a 10-day pre-proposal window and a 60-day public comment period first. Final rules are meant to land alongside the GENIUS Act, and licensed issuers get a one-year transition.

Is my USDC safer under the new reserve rules?

On the reserve side, yes. The ban on rehypothecation, the multi-custodian requirement, and the two-business-day redemption rule all reduce the chance of a reserve shortfall or a depeg for token holders.