$5.9B USDe Pays 4% Yield, Skirts GENIUS Act Ban

Key Points

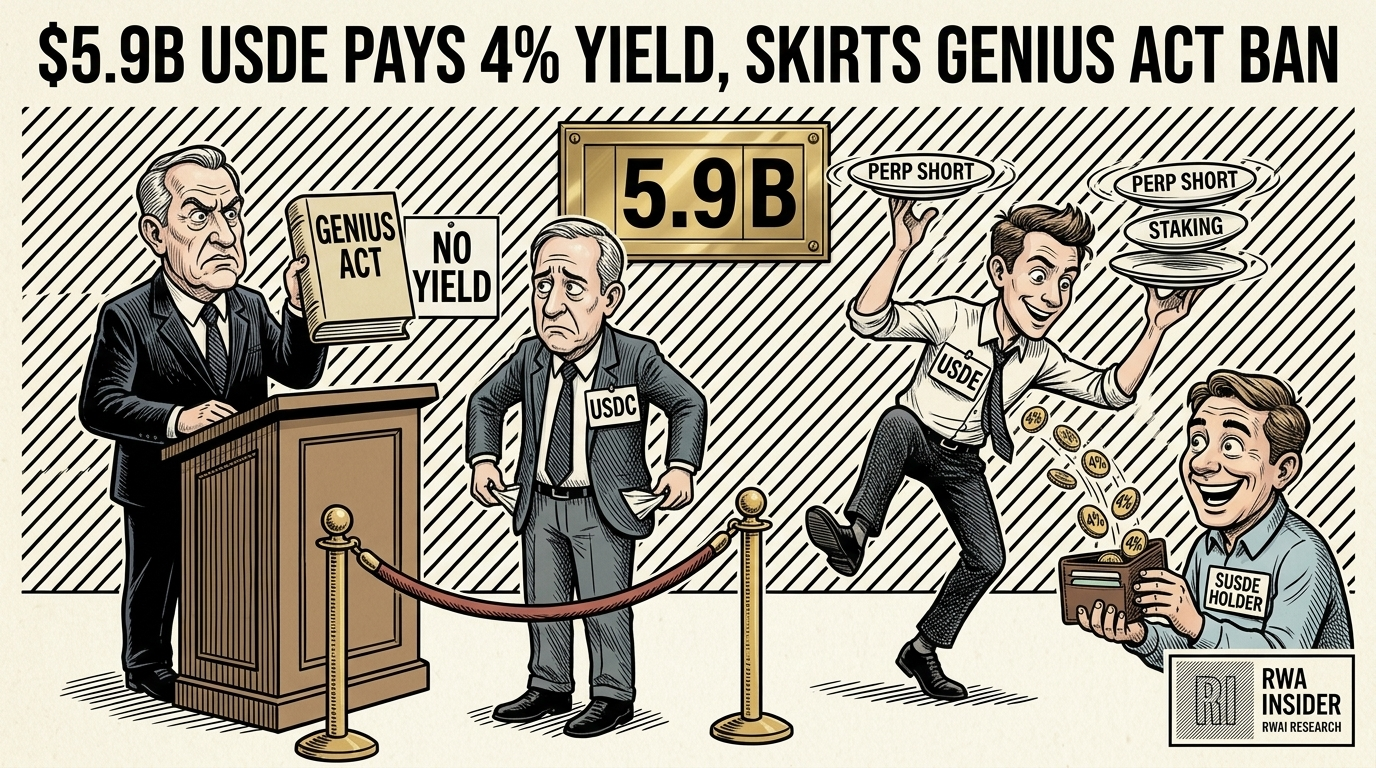

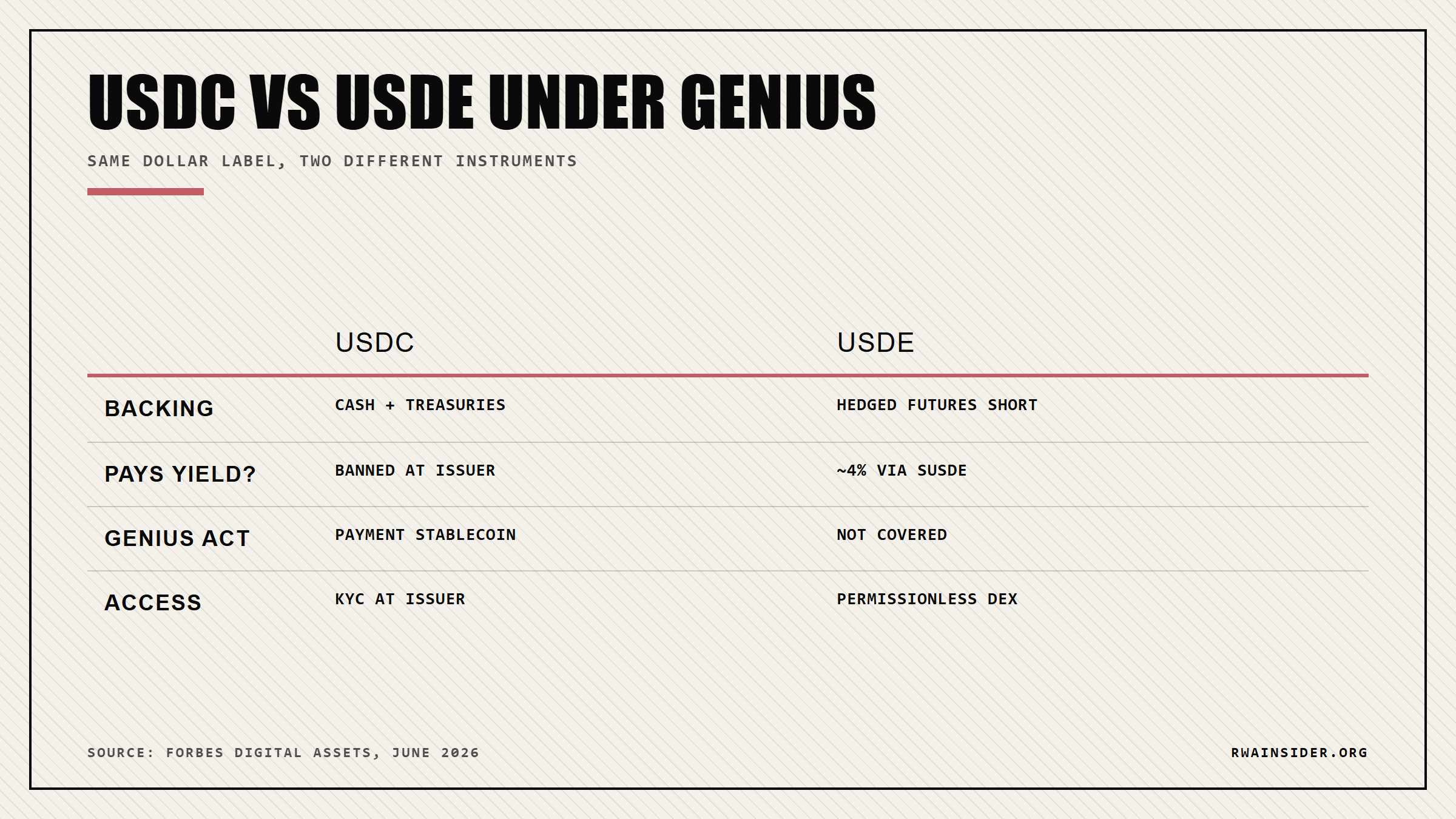

- USDe pays roughly 4% staked yield in 2026 while the GENIUS Act bars USDC and other payment stablecoins from paying holders any yield at all.

- USDe supply peaked above $14 billion in 2025 at about 5% of the stablecoin market, the only non-fiat-backed dollar near the top.

- Any wallet can buy USDe on a DEX and stake it as sUSDe for yield, but the peg dipped to $0.97 in October 2025.

Ethena’s USDe now holds around $5.9 billion in supply and still pays holders close to 4% a year, even though the GENIUS Act tells every payment stablecoin issuer it cannot pay holders “any form of interest or yield.” Forbes Digital Assets contributor Zennon Kapron explains why that clause never reaches USDe: it is a delta-neutral synthetic dollar backed by a hedged futures trade, not cash in a bank. For a wallet holder, that gap is the entire story, because the yield USDC can no longer pay legally still flows to anyone who stakes USDe as sUSDe.

Why The GENIUS Act Yield Ban Misses USDe

When Congress wrote the GENIUS Act, it drew one hard line: a payment stablecoin issuer cannot pay holders interest or yield.

That clause forced Circle and Coinbase to rebuild how USDC holders earn. The biggest yield-bearing dollar in crypto steps around it completely.

Ethena built USDe to decline that definition. It does not hold cash or Treasuries.

Instead, the protocol takes crypto collateral and opens an offsetting short in perpetual futures, so the dollar value stays roughly flat while the position earns.

Stake USDe as sUSDe and you collect that return on-chain, permissionless, with no issuer paying a cent of interest. The clause that reshaped USDC never touches it.

That makes USDe a rare dollar that earns without an issuer balance sheet behind it, and the rulebook simply has no box to put it in.

Where USDe’s 4% Yield Actually Comes From

The return is a cash-and-carry basis trade, the oldest structure in derivatives. When perpetual funding rates are positive, long positions pay shorts.

USDe’s hedged short collects that flow on top of the staking yield its collateral already earns. In early 2026, the staked token paid around 4% a year.

Strip away the regulatory framing and this is really about whether a wallet should price a derivatives position the way it prices a checking account.

The size is real. USDe supply peaked above $14 billion in 2025, near 5% of the whole stablecoin market, and CoinDesk called it the third-largest dollar-denominated crypto asset.

After an October 2025 deleveraging, supply settled near $5.9 billion, where it sits today. Even shrunk, it is the only non-fiat dollar anywhere near the top of the table.

For comparison, plain USDC supplied to Aave earns roughly 2% today, and under GENIUS the issuer itself can legally add nothing on top.

That spread is why the synthetic dollar keeps pulling deposits, and you can track how stablecoin yields keep shifting across DeFi as Washington tightens the rules.

BaFin Bans USDe While Janus Henderson Buys In

Regulators are not converging. Germany’s BaFin forced Ethena to wind down its local entity and banned public USDe sales, calling it an unregistered security under MiCA’s reserve rules.

That made Ethena the third stablecoin issuer pushed out of the EU. US institutions went the other way, treating the synthetic dollar as infrastructure rather than a threat.

In June 2026, Janus Henderson, with about $480 billion under management, partnered with Ethena to use USDe for treasury cash management and fold its tokenized AAA credit into the reserves.

Forbes contributor Zennon Kapron frames the split bluntly: one major market treats the synthetic dollar as an unregistered security, while another wires it into the plumbing of a half-trillion-dollar asset manager.

The OCC’s March 2026 proposal would extend the yield ban to affiliates and third parties, but it aims at issuers paying yield through a side door, not an instrument that pays none.

USDe added Kraken as a custody partner in January 2026 with weekly proof-of-reserves, yet the real risk is a long negative-funding window hitting during a leveraged unwind, exactly what dragged it to $0.97 last October.

Whether USDe’s 4% holds depends on funding rates staying positive and on Washington deciding if synthetic dollars deserve their own rulebook. Until a regulator draws that perimeter, the yield keeps migrating to whatever sits just outside the line GENIUS already drew.

Watching the rulebook take shape on stablecoin yield? See how the same OCC proposal already threatens Coinbase’s USDC rewards.

Frequently Asked Questions

What is Ethena’s USDe and how does it earn yield?

USDe is a delta-neutral synthetic dollar from Ethena. It backs each token with crypto collateral plus an offsetting short in perpetual futures, then passes the funding-rate and staking return to anyone who stakes it as sUSDe.

Does the GENIUS Act let USDe pay yield?

The GENIUS Act only bans yield for payment stablecoins backed one-to-one by cash and Treasuries, like USDC. USDe is not built that way, so the ban does not reach it, and sUSDe still paid around 4% in early 2026.

Can I buy and stake USDe without going through an issuer?

Yes. USDe trades permissionlessly on DEXes and stakes as sUSDe fully on-chain, with no issuer paying interest. Europe is the exception, since BaFin banned public USDe sales under MiCA.

How risky is USDe’s yield compared to a normal stablecoin?

It carries a different risk. The yield depends on funding rates staying positive, and Ethena’s own data shows 17.5% of days ran negative over three years. USDe briefly slipped to $0.97 during the October 2025 flash crash before recovering.