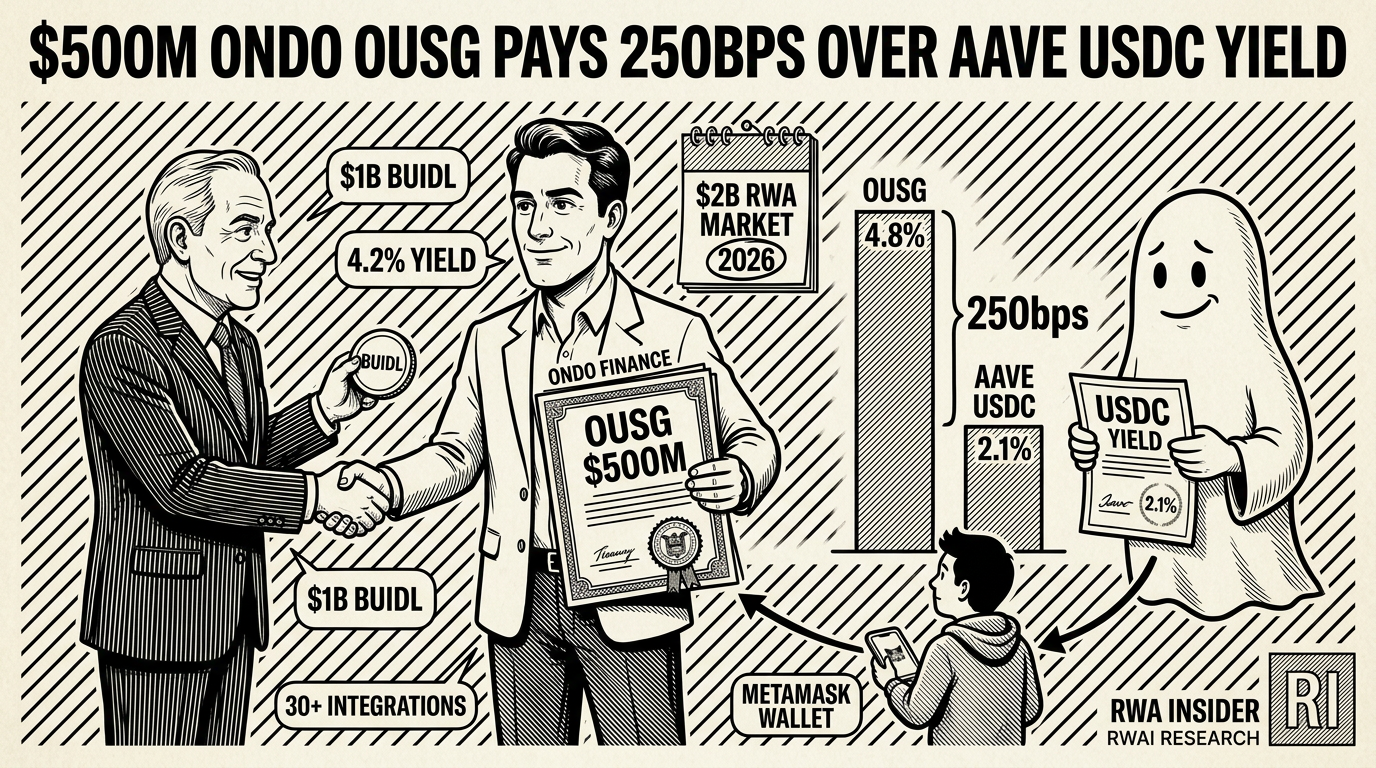

$500M Ondo OUSG Pays 250bps Over Aave USDC Yield

Key Points

- Ondo Finance’s OUSG product crossed $500 million in outstanding tokens, with the broader on-chain tokenized RWA market now passing $2 billion in total value.

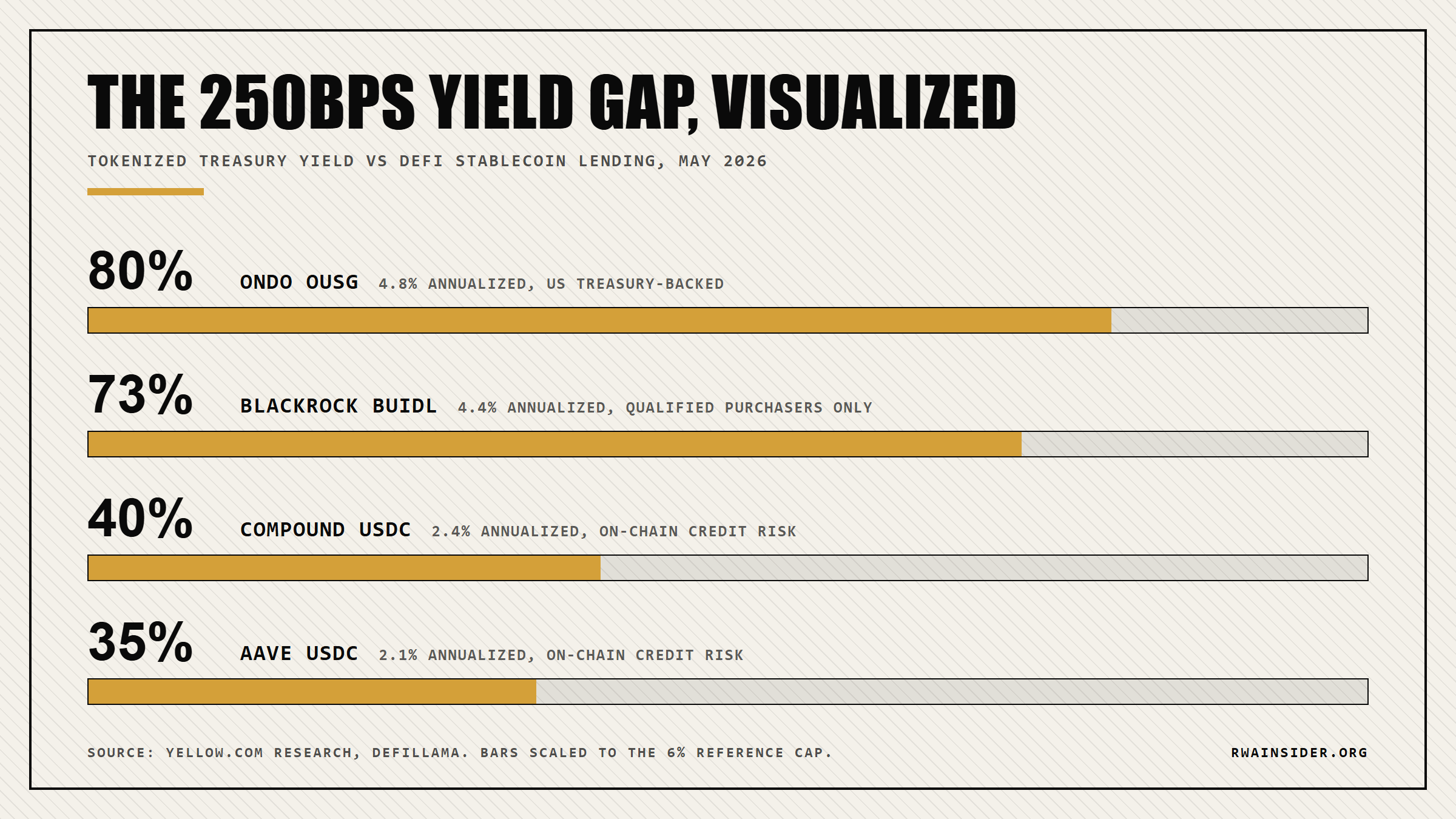

- Short-duration tokenized US Treasuries currently yield between 4.2% and 5.4%, while USDC on Aave or Compound has oscillated between 2% and 4% over the same window.

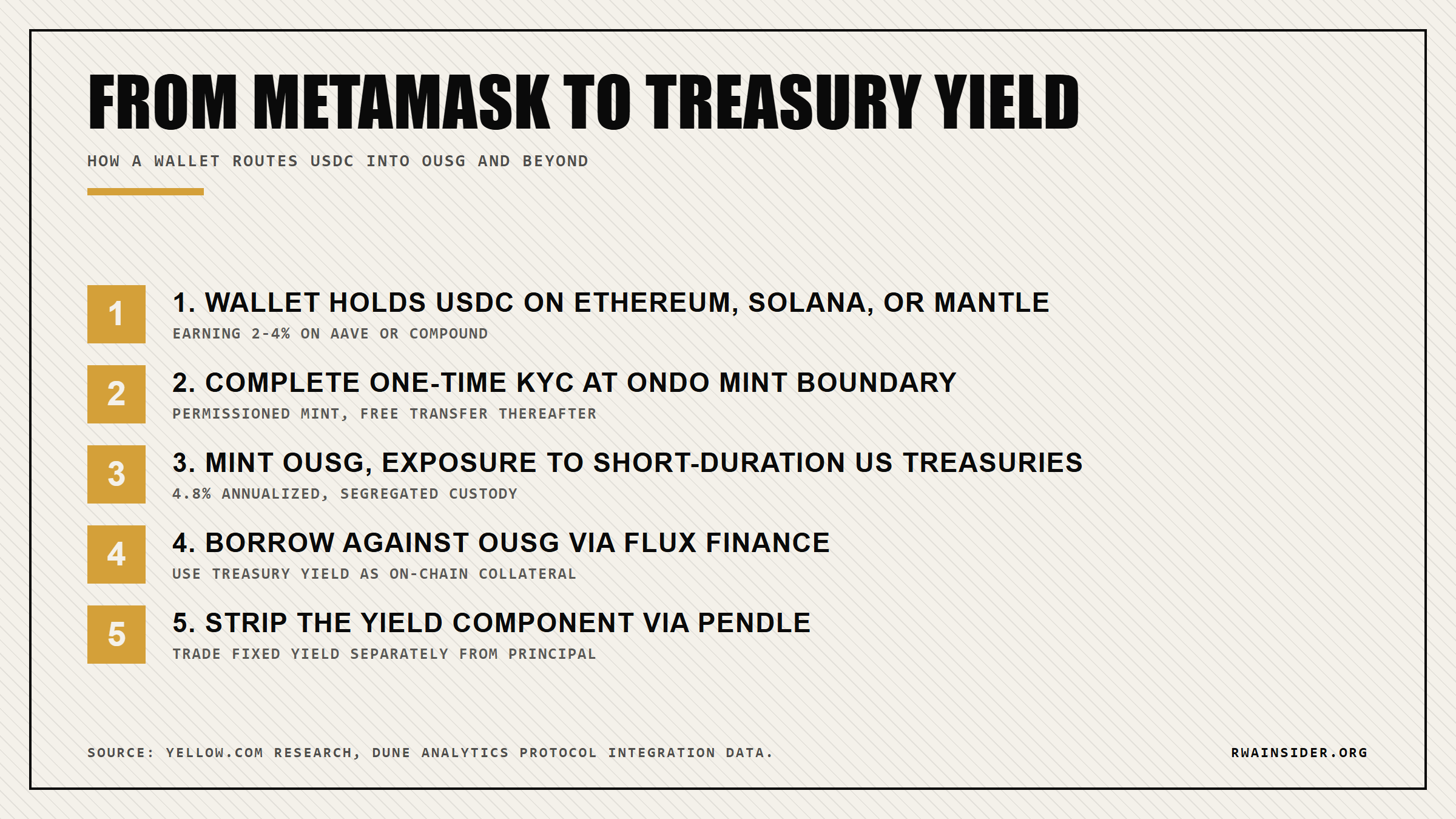

- Any DeFi wallet on Ethereum, Solana, or Mantle can rotate stablecoins into OUSG or USDY after a one-time KYC, then borrow against the position through Flux Finance.

Ondo Finance now holds the largest share of tokenized US Treasury product supply on-chain, with its OUSG wrapper crossing $500 million in outstanding tokens as the broader RWA market passes $2 billion in total value. The data comes from a research note published this week by Yellow.com tracking on-chain Treasury flows and protocol TVL across the sector. For a DeFi user sitting in stablecoins, the move signals a structural yield arbitrage: short-duration tokenized Treasuries pay 4.2% to 5.4%, while USDC on Aave and Compound oscillates between 2% and 4%, leaving up to 250 basis points on the table.

How Ondo Built The $2B Tokenized Treasury Lead

Ondo Finance‘s OUSG is a tokenized wrapper around short-duration US Treasury ETFs, originally backed by the BlackRock iShares Short Treasury Bond ETF and now partially backed by the BUIDL fund.

According to Yellow.com’s research note, OUSG and Ondo’s USDY together “represent the most accessible institutional-grade access layer” for tokenized US Treasury exposure on public chains today.

USDY, Ondo’s second flagship product, is a yield-bearing instrument designed for non-US wallets under applicable securities frameworks.

The protocol’s permissioned-mint, free-transfer architecture is the design choice that separated Ondo from earlier tokenized-security attempts.

KYC happens once at the mint or redeem boundary, then the token moves freely between wallets and DeFi contracts on Ethereum, Solana, and Mantle.

That model collapsed the secondary-market friction that had blocked prior tokenized debt products on-chain.

Ondo also operates Flux Finance, a lending market that lets OUSG holders borrow stablecoins against their Treasury position.

That turns a passive yield-bearing token into a leveraged collateral asset, the bridge between institutional yield and DeFi composability.

Where The 250bps Yield Gap Comes From

The arithmetic is direct. Short-duration US Treasury instruments have yielded between 4.2% and 5.4% annualized since mid-2023, depending on duration.

USDC on Aave or Compound has oscillated between 2% and 4% over the same window, and the rate drops sharply when borrowing demand thins during low-volatility regimes.

Bitcoin’s current nine-month volatility low is exactly that kind of regime.

A wallet holding $10,000 in USDC on Aave at today’s 2.1% earns roughly $210 per year.

The same $10,000 rotated into OUSG at 4.8% earns $480, a difference of $270 per year on a relatively small position.

For a DeFi user, this matters less as an institutional product launch than as a direct annualized return on every dollar idle in a stablecoin money market.

Tracking how this gap moves week to week across Ondo, Superstate, Hashnote, and Franklin Templeton sits at the core of our DeFi-native yield coverage on RWA Insider.

The risk profile is also different: OUSG is backed by direct government obligations held in segregated custody, while stablecoin lending exposes the wallet to anonymous borrower default and protocol smart-contract risk.

Tokenized Treasuries shift the risk anchor from on-chain credit to sovereign debt.

Where Composability Locks In The Ondo Advantage

The competitive moat for Ondo is not the Treasury wrapper itself; Superstate, Backed Finance, and OpenEden all build similar instruments.

The moat is composability depth. Morpho lists OUSG and USDY as collateral types.

Pendle Finance has built yield-stripping markets that let users trade the fixed yield component separately from the principal of a tokenized Treasury.

That structure is an on-chain interest rate swap on top of a Treasury token, a layer that would require multiple intermediaries and T+2 settlement in traditional markets.

Robert Leshner, the former Compound chief executive now leading Superstate, has positioned the rival USTB fund for institutional direct subscribers rather than DeFi composability, a deliberately different bet than Ondo’s.

Dune Analytics data shows OUSG and USDY now appear as collateral or yield source components in over 30 distinct DeFi protocols and dashboards, up from fewer than five in early 2024.

Boston Consulting Group’s widely cited 2022 analysis projected the tokenized illiquid asset market could reach $16 trillion by 2030, a 50-fold scale jump from current on-chain levels.

That number depends on legal standardization, regulated custody at scale, and central exchange acceptance of tokenized collateral, three developments that are in progress but not complete.

Whether the next wave of DeFi capital migrates from USDC money markets to tokenized Treasuries depends on KYC tolerance and how fast the composability stack thickens around Ondo’s products.

For wallets tracking the chain map of tokenized Treasury flow, our companion read on BUIDL’s Solana expansion and BlackRock’s multi-chain Treasury push covers which networks the institutional rail is reaching first.

Frequently Asked Questions

What is Ondo Finance OUSG and how does it tokenize US Treasuries?

OUSG is Ondo Finance’s tokenized wrapper around short-duration US Treasury ETF exposure, originally backed by the BlackRock iShares Short Treasury Bond ETF and now partially backed by BlackRock’s BUIDL fund. Tokens are minted after a one-time KYC at the protocol boundary, then transfer freely on Ethereum, Solana, and Mantle. The on-chain token represents a claim on the underlying off-chain Treasury position held in segregated custody.

How much yield does Ondo OUSG offer compared to Aave USDC?

OUSG currently yields between 4.2% and 5.4% annualized, tracking short-duration US Treasury rates. USDC on Aave has oscillated between 2% and 4% over the same period, with the spread widening when DeFi borrowing demand thins. On a $10,000 position, that gap is roughly $270 of additional annual yield in favor of OUSG.

Can I buy Ondo OUSG without KYC?

No. OUSG requires KYC and AML verification at the mint and redemption boundary because it is structured as a regulated security wrapper. Once minted, the token transfers freely on-chain between wallets and DeFi contracts, but the initial onboarding step is permissioned. Non-US wallets that prefer to avoid US securities frameworks can hold USDY, Ondo’s yield-bearing instrument designed for that audience.

How does Ondo work with BlackRock BUIDL?

Ondo integrated BUIDL as a partial backing asset for OUSG, which effectively makes the Ondo protocol a DeFi-accessible distribution layer for BlackRock’s institutional money-market fund. BlackRock handles the regulated custody and fund operations on the BUIDL side. Ondo handles the DeFi-native distribution and composability layer on the on-chain side, including integration with Flux Finance, Morpho, and Pendle.