Ethereum Anchors $15B RWA Lead As Solana, XRP Specialize

Key Points

- Ethereum hosts $15 to $17 billion in tokenized real-world assets, anchored by BlackRock’s BUIDL and Franklin Templeton’s tokenized money market products.

- Solana briefly surpassed Ethereum in RWA holders by pushing low-fee execution, while XRP Ledger anchors banking rails via ISO 20022 compatibility.

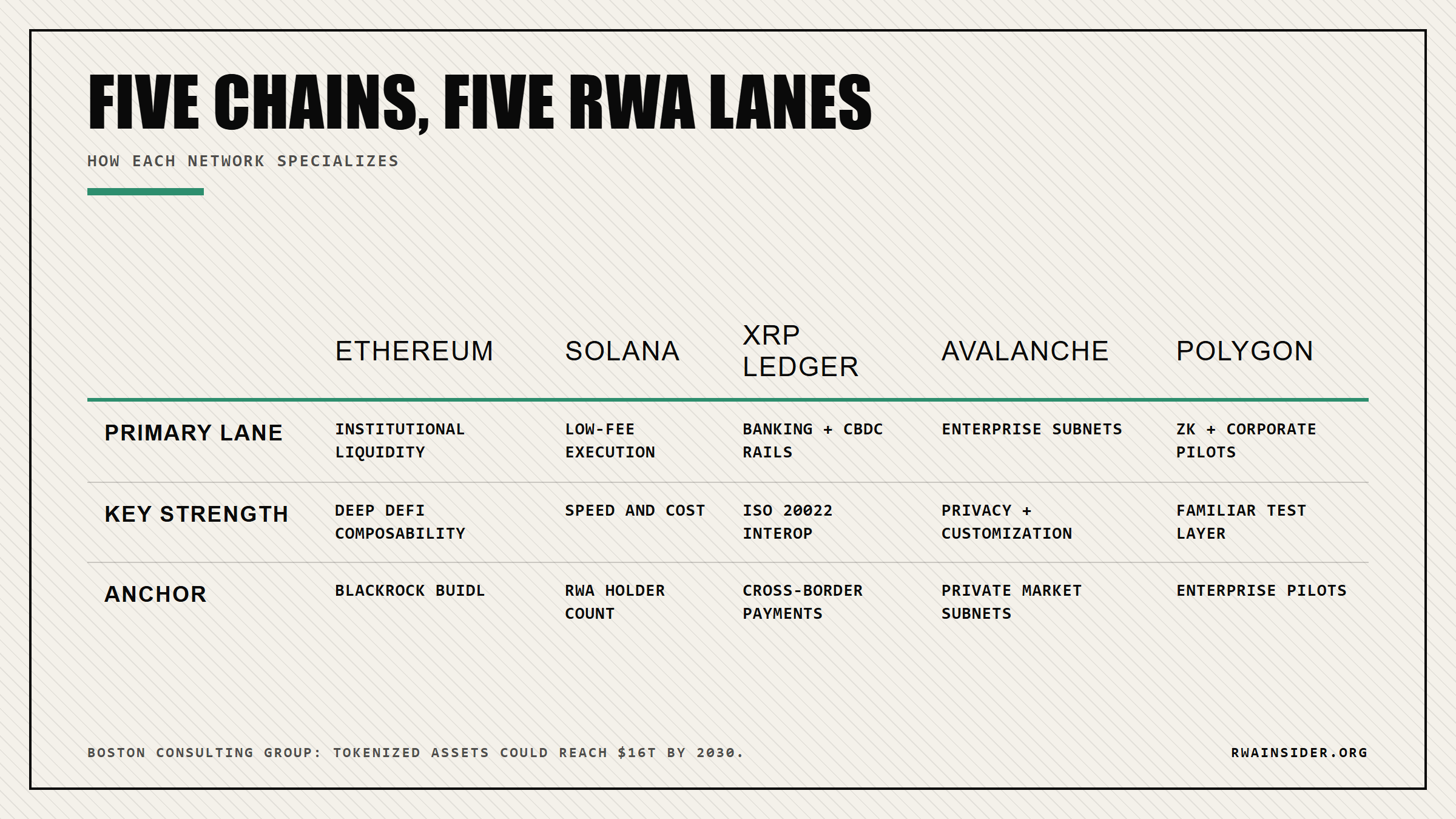

- DeFi users now choose chains by lane: Ethereum for liquidity, Solana for cost, XRP Ledger for payments, Avalanche for subnets, Polygon for ZK pilots.

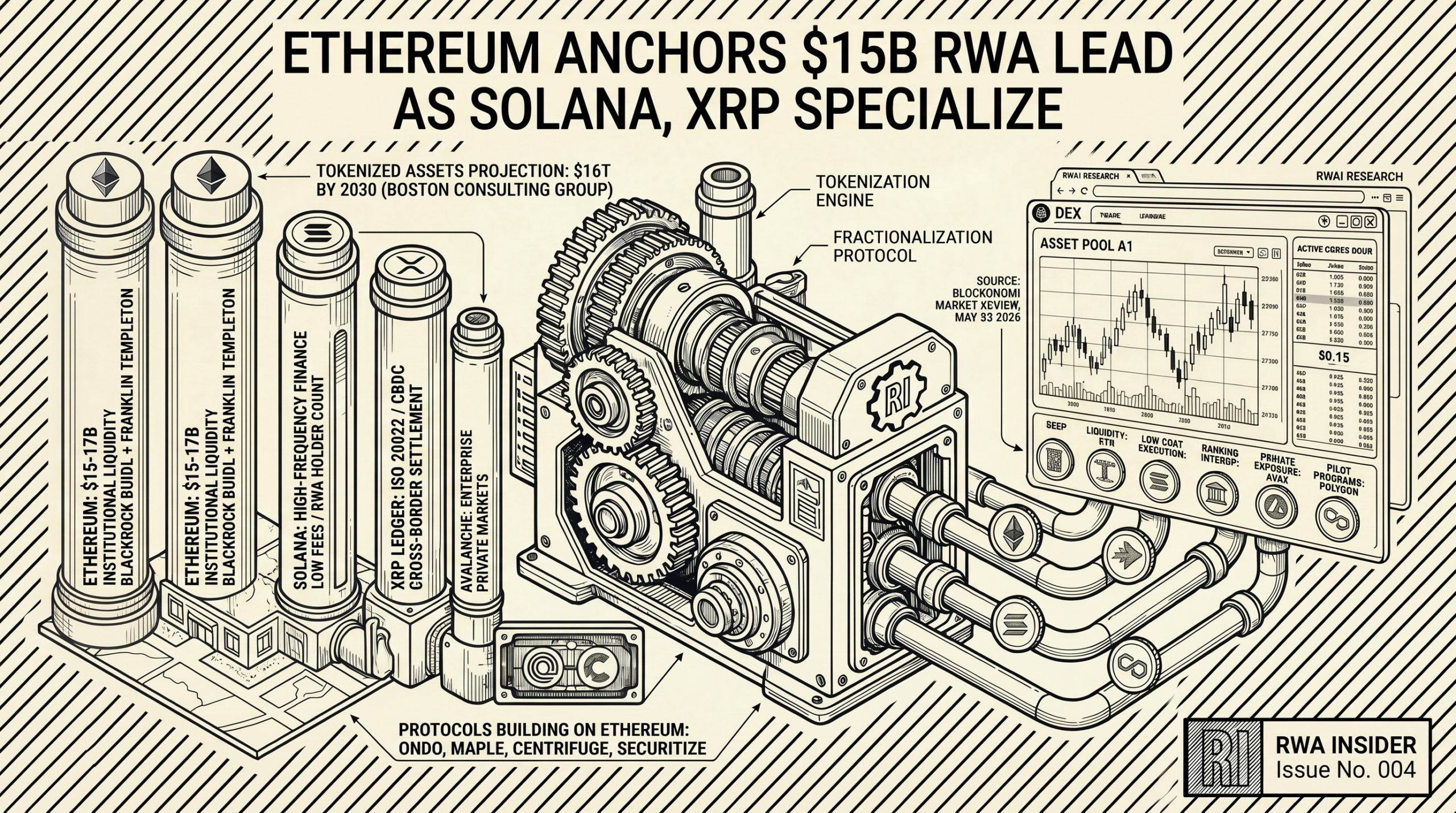

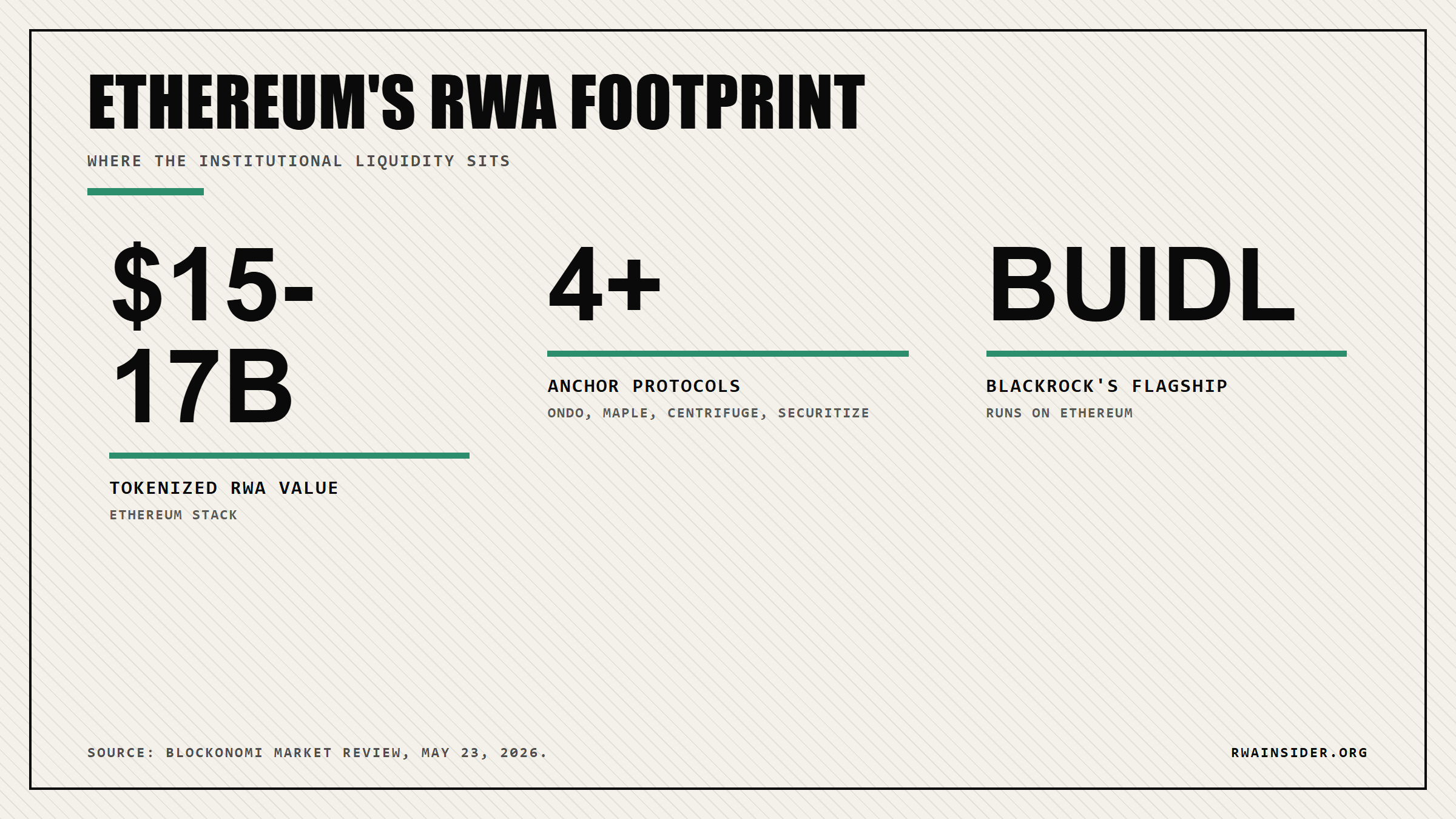

Ethereum’s tokenized real-world asset stack sits between $15 billion and $17 billion, anchored by BlackRock’s BUIDL fund, Franklin Templeton’s tokenized products, and protocols including Ondo Finance, Maple Finance, Centrifuge, and Securitize. Blockonomi mapped the competitive landscape on May 23, 2026, framing the RWA race as fragmentation rather than winner-take-all. For a wallet deciding where to deploy stablecoin capital, the choice is no longer one chain but five: Ethereum for liquidity, Solana for cost, XRP Ledger for banking rails, Avalanche for enterprise subnets, and Polygon for zero-knowledge pilots.

Ethereum’s $15B Stack Holds The Institutional RWA Liquidity

Blockonomi wrote that “RWA market competition is entering a decisive phase as major blockchain networks compete for institutional financial infrastructure.”

Ethereum‘s tokenized asset ecosystem sits between $15 billion and $17 billion in current value, per the Blockonomi review.

BlackRock’s BUIDL fund and Franklin Templeton’s tokenized products both run on Ethereum.

Protocols including Ondo Finance, Maple Finance, Centrifuge, and Securitize have strengthened Ethereum’s institutional position during the latest expansion cycle.

The network keeps benefiting from deep liquidity pools and composability across decentralised finance. The trade-off is operational cost and scalability, which is exactly where every other chain is now targeting.

Solana’s Cost Edge, XRP Ledger’s Banking Rails, Avalanche Subnets

Solana is targeting Ethereum’s cost weakness directly. The network briefly surpassed Ethereum in total RWA holders during the recent expansion cycle.

Solana’s bet is simple: lower fees and faster settlement will attract larger liquidity pools over time.

The competition is more on execution efficiency than on trust or composability.

XRP Ledger took a different lane. The network focuses on interbank settlement and ISO 20022 compatibility for cross-border payments and CBDC integration, explicitly avoiding direct competition with public DeFi markets.

Strip away the chain wars and this is really about which lane fits a $1k wallet’s actual strategy, not which chain wins the headline race.

Readers can compare RWA infrastructure across chains as the lanes specialize further.

Avalanche’s subnet architecture lets institutions run isolated blockchain environments with privacy controls.

That model continues attracting enterprise experimentation around tokenized financial products and private market infrastructure, where firms prefer not to expose sensitive activity to fully public networks.

Polygon positions as the accessible institutional entry layer through zero-knowledge scaling and corporate pilots. Traditional firms continue using Polygon to test tokenized financial products without abandoning existing operational frameworks.

BCG’s $16T By 2030 Projection And What It Means For Wallets

The numerical hook framing this competition is Boston Consulting Group’s projection that tokenized assets could approach $16 trillion by 2030.

That number accelerates the race. Different networks are now specializing across liquidity, settlement, payments, scalability, and enterprise integration rather than competing for one universal use case.

For wallets actively allocating stablecoin capital, the practical read is that “chain choice” no longer means picking the winner.

It means picking the lane that fits the asset.

Yield-bearing stablecoin products built on Ethereum, including BlackRock BUIDL and Franklin Templeton’s tokenized money market, suit liquidity-heavy strategies and DeFi composability.

High-frequency trading and small-position rebalancing favour Solana’s lower fees. Cross-border payment exposure aligns more naturally with XRP Ledger’s settlement focus and ISO 20022 hooks.

Avalanche’s enterprise subnets suit private institutional exposure where the wallet wants reduced public visibility. Polygon’s zk pilots suit transitional treasury operations testing tokenization without committing to a single L1.

For now the early signal is clear. Capital is not consolidating onto one L1 but spreading across lanes that match issuer needs, custody requirements, and target user behaviour.

The forward question is whether any single chain captures dominant share of the $16 trillion projection by 2030, or whether the specialization persists and the RWA market stays multi-chain by design.

Whether the lane-specialization model holds depends on whether one chain breaks out across multiple categories, or whether the institutional capital deliberately spreads to match risk profiles. The next 30-day snapshots will start to tell.

Track more Secondary Markets coverage from RWA Insider as the multi-chain RWA league table reshuffles.

Frequently Asked Questions

Which blockchain holds the most tokenized RWAs?

Ethereum still holds the largest tokenized real-world asset stack at $15 to $17 billion. BlackRock’s BUIDL fund, Franklin Templeton’s tokenized products, and protocols including Ondo Finance, Maple Finance, Centrifuge, and Securitize all anchor Ethereum’s institutional position.

How does Solana compete with Ethereum for RWA share?

Solana competes on execution efficiency rather than trust. The network briefly surpassed Ethereum in total RWA holders by pushing lower fees and faster transaction settlement. The bet is that high-frequency financial applications will migrate to Solana over time.

Why is XRP Ledger pursuing banking rails instead of DeFi?

XRP Ledger has positioned itself as a messaging and settlement layer for global finance, with ISO 20022 compatibility for traditional banking interoperability. CBDC discussions and cross-border payment integrations remain central to its strategy. The network has explicitly avoided direct competition with public DeFi markets.

How big could the tokenized asset market get by 2030?

Boston Consulting Group estimates tokenized assets could approach $16 trillion by 2030. That projection accelerates competition among blockchain ecosystems pursuing different segments: liquidity, settlement, payments, scalability, and enterprise integration.