$211B RWA Perps Hit Record As CEX Spot Cools

Key Points

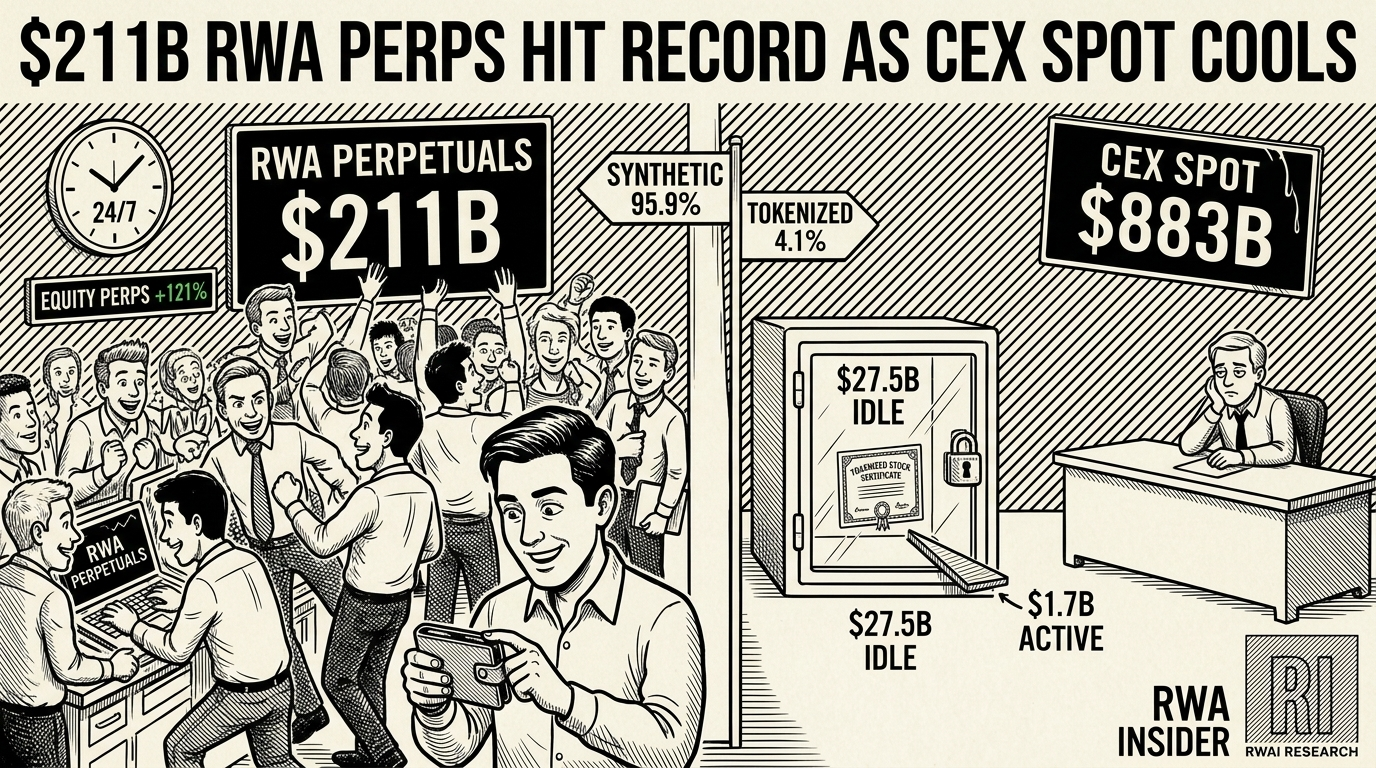

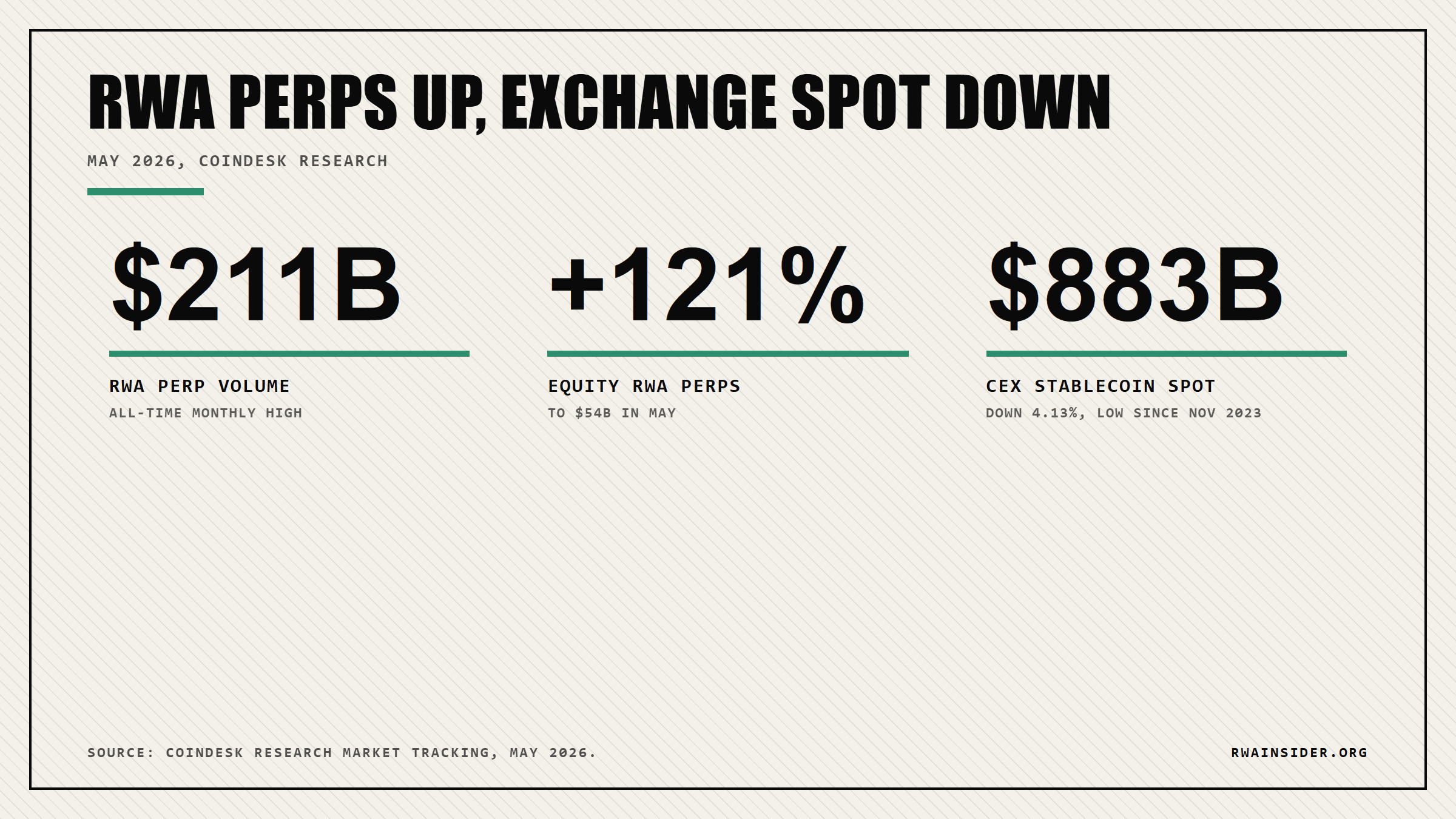

- CoinDesk Research data show real-world asset perpetual volume reached a record $211 billion in May 2026, with equity perps alone up 121% to $54 billion.

- Centralized exchange stablecoin spot activity fell 4.13% to $883 billion over the same month, its lowest level since November 2023.

- Any wallet can trade these RWA perps for round-the-clock exposure to stocks and Treasuries, yet only 4.1% settle on tokenized contracts.

Traders pushed real-world asset perpetual volume to a record $211 billion in May 2026, even as spot order books across centralized exchanges thinned out. CoinDesk Research data put equity RWA perps up 121% to $54 billion for the month, while stablecoin spot activity, a proxy for centralized exchange trading, slid 4.13% to $883 billion, the lowest reading since November 2023. For a wallet, the signal is direct: round-the-clock exposure to stocks, Treasuries, and commodities now lives in crypto-native derivatives, not in the tokenized assets sitting idle on-chain.

RWA Perps Hit $211B As Traders Skip Spot

In May, while order books for major tokens thinned, traders piled into RWA perpetuals chasing clean execution and round-the-clock exposure to equities, Treasuries, and commodities on crypto rails.

Data from CoinDesk Research put total RWA perp volume at a record $211 billion, with equity perps alone climbing 121% to $54 billion in a single month.

Over the same stretch, centralized exchange stablecoin spot activity fell 4.13% to $883 billion, the quietest it has been since November 2023.

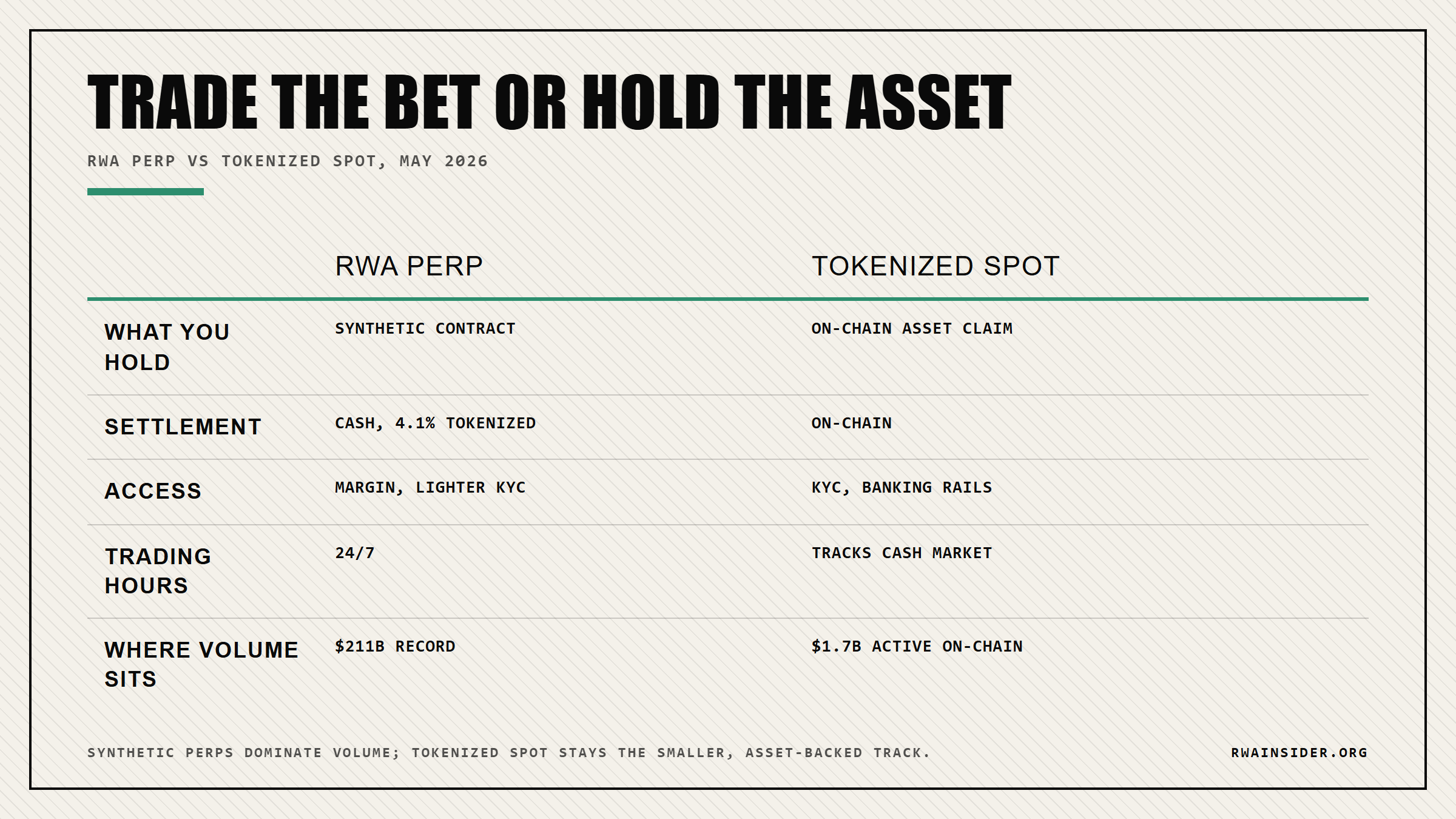

An RWA perp is a crypto-native perpetual contract that tracks a traditional asset, a stock index or a Treasury proxy, without an expiry date.

The draw is simple. Perps stay open when the underlying equity and bond markets close, so a wallet can hold the exposure overnight, on weekends, and through macro data prints.

Only 4.1% Of RWA Perps Settle On-Chain

Here is the catch behind the RWA label. Only 4.1% of RWA perp volume settles on tokenized contracts, according to a May market scan from CoinMarketCap Research.

The rest are cash-settled synthetics. You are trading a derivative that references a TradFi index, not taking delivery of a tokenized share or bond you can hold in a wallet.

Strip away the RWA label and most of this volume is a synthetic bet on a price feed, not a claim on a real asset parked on-chain.

The tokenized assets themselves tell the other half of the story.

Tokenized RWA outstanding stood near $27.5 billion in May, but only about $1.7 billion was actively used as DeFi collateral or lending, per Dune data.

That leaves a two-track market: tens of billions parked passively in reserves, and a thin slice actually changing hands on-chain. Traders went where the liquidity already was.

On-chain venues are not standing still.

Nansen figures cited by CryptoBriefing show on-chain perpetual platforms processed more than $2 trillion in the first quarter of 2026, with one venue alone handling over $625 billion.

For a wider view of how these markets are maturing, we track liquidity shifts across RWA secondary markets as synthetic and tokenized rails compete.

Why Tokenized Settlement Still Trails Volume

The shift fits a pattern the market has been signaling for months.

Gracy Chen, chief executive of Bitget, argued in earlier coverage that tokenized markets have moved past a race over access and into a race over efficiency.

Her point lands here. Liquidity migrates to whatever instrument trades cheapest, and right now that is the synthetic perp, not the tokenized share.

We covered that same liquidity race playing out on exchange order books.

What to watch is whether tokenized settlement, stuck at 4.1%, and on-chain collateral, near $1.7 billion of $27.5 billion, catch up enough that traders can hold the asset instead of just renting a price feed.

The risks are specific. Index or oracle errors can misprice a perp when the underlying cash market is closed, and funding rates can swing hard around earnings, auctions, and macro data.

Regulation is the other shoe. A ruling on synthetic equity or rate exposure could thin out listings or cut access for some wallets overnight.

Access today is the perp’s edge. Retail can trade these contracts around the clock with lighter onboarding than tokenized spot, which still leans on KYC and banking rails.

Whether RWA perps stay the deepest market depends on tokenized settlement closing the gap with synthetic volume. Until it does, the record belongs to the derivative, not the asset it tracks.

If you trade RWA perps, watch the funding rate and the reference index as closely as the price, because that is where the round-the-clock edge can quietly turn against you.

Frequently Asked Questions

What are RWA perpetuals?

RWA perpetuals are crypto-native perpetual contracts that track a traditional asset like an equity index, a Treasury proxy, or a commodity, with no expiry date. Most are cash-settled against a price index rather than delivering a tokenized share or bond you hold in a wallet.

Why did RWA perp volume hit $211 billion while exchange spot fell?

Perps offer leverage, tight execution, and 24/7 access, so traders kept their exposure even as spot cooled. CoinDesk Research recorded RWA perp volume at a record $211 billion in May, while centralized exchange stablecoin spot slid 4.13% to $883 billion, the lowest since November 2023.

Can I trade RWA perps without holding the tokenized asset?

Yes. About 95.9% of RWA perp volume is synthetic, meaning you trade a contract that references the asset’s price rather than the asset itself. Only 4.1% settles on tokenized contracts, according to CoinMarketCap Research.

Are RWA perps risky for a small wallet?

They carry leverage, funding-rate swings, and oracle risk when the underlying cash market is closed. A bad index tick or a funding spike around macro data can move a position fast, so size carefully and watch the reference index, not just the headline price.